Electronics Market: Favorable Pricing and Stock Availability Overshadowed by Lead Time Volatility in June

Lytica is the world’s only provider of electronic component spend analytics and risk intelligence using real customer data. As a result of our unique position in the marketplace, we’ve been able to work with 100+ customers in analyzing over $500 billion in electronics spend. We’ve curated up-to-date insights on the state of the electronic component market and will be sharing them with you each month.

Lytica’s component basket of goods used in our analysis is comprised of 165,000 electronic components across more than 30 categories, consisting of the most popular devices used by our customers. These indices are intended to show trends in the market. Individual component and BoM analysis is offered by Lytica as a service to our customers.

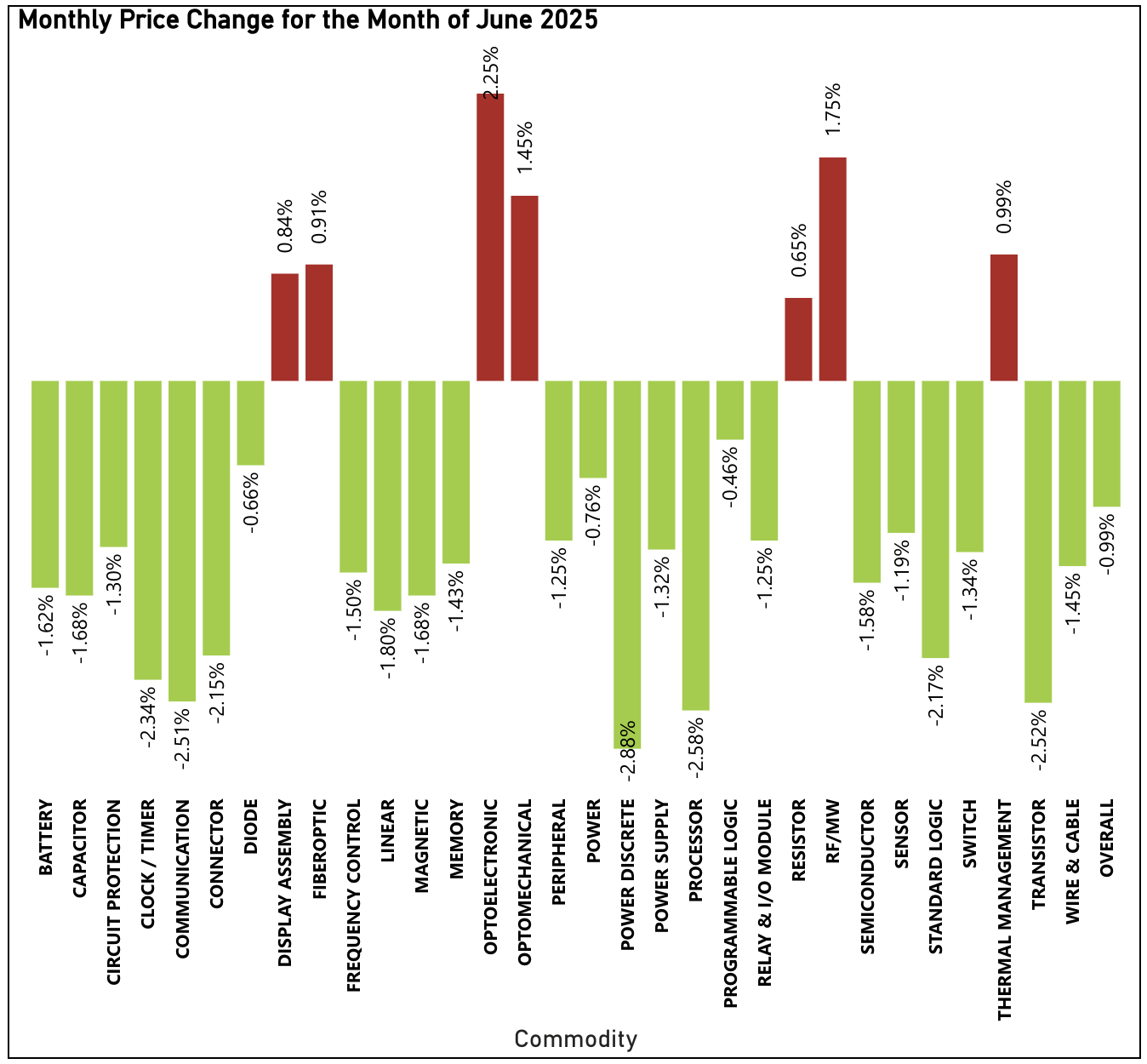

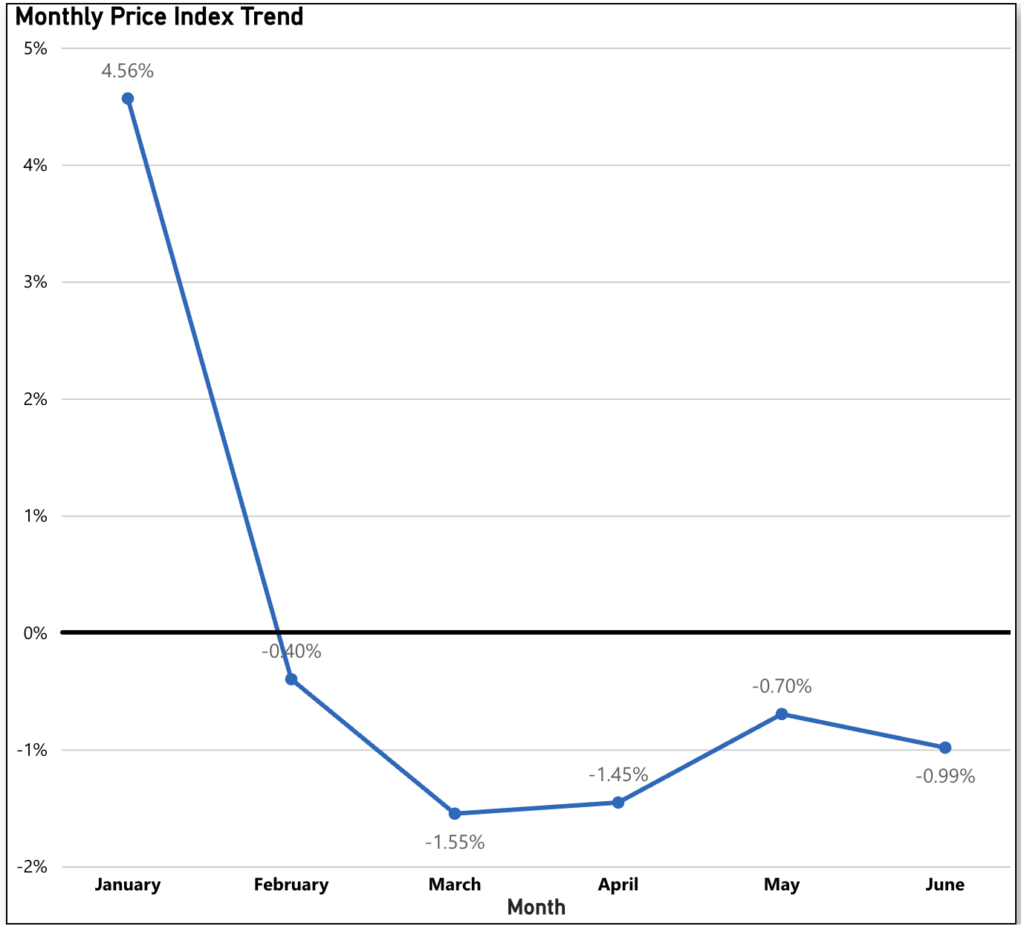

Decreasing Prices Continue for Fifth Consecutive Month in June

Component prices extended their downward trend in June, marking the fifth straight month of declines. The average drop of 0.99%, a steeper decline than May’s 0.70%, remains more moderate than March (-1.55%) and April (-1.45%), but continues to signal a clear shift toward a buyer’s market. Procurement teams are seeing sustained pricing leverage across a range of categories, reinforcing the favorable conditions that began taking shape earlier in the year.

The biggest drivers in this pricing readout include Power Discrete (down 2.88% month-to-month), Processor (down 2.58% month-to-month), Transistor (down 2.52% month-to-month) and Communication (down 2.51% month-to-month). All but 7 commodities noted price decreases in the month of May.

The commodities pushing upward against this trend include Optoelectronic (up 2.25% month-to-month), RF/MW (up 1.75% month-to-month), and Optomechanical (up 1.45% month-to-month).

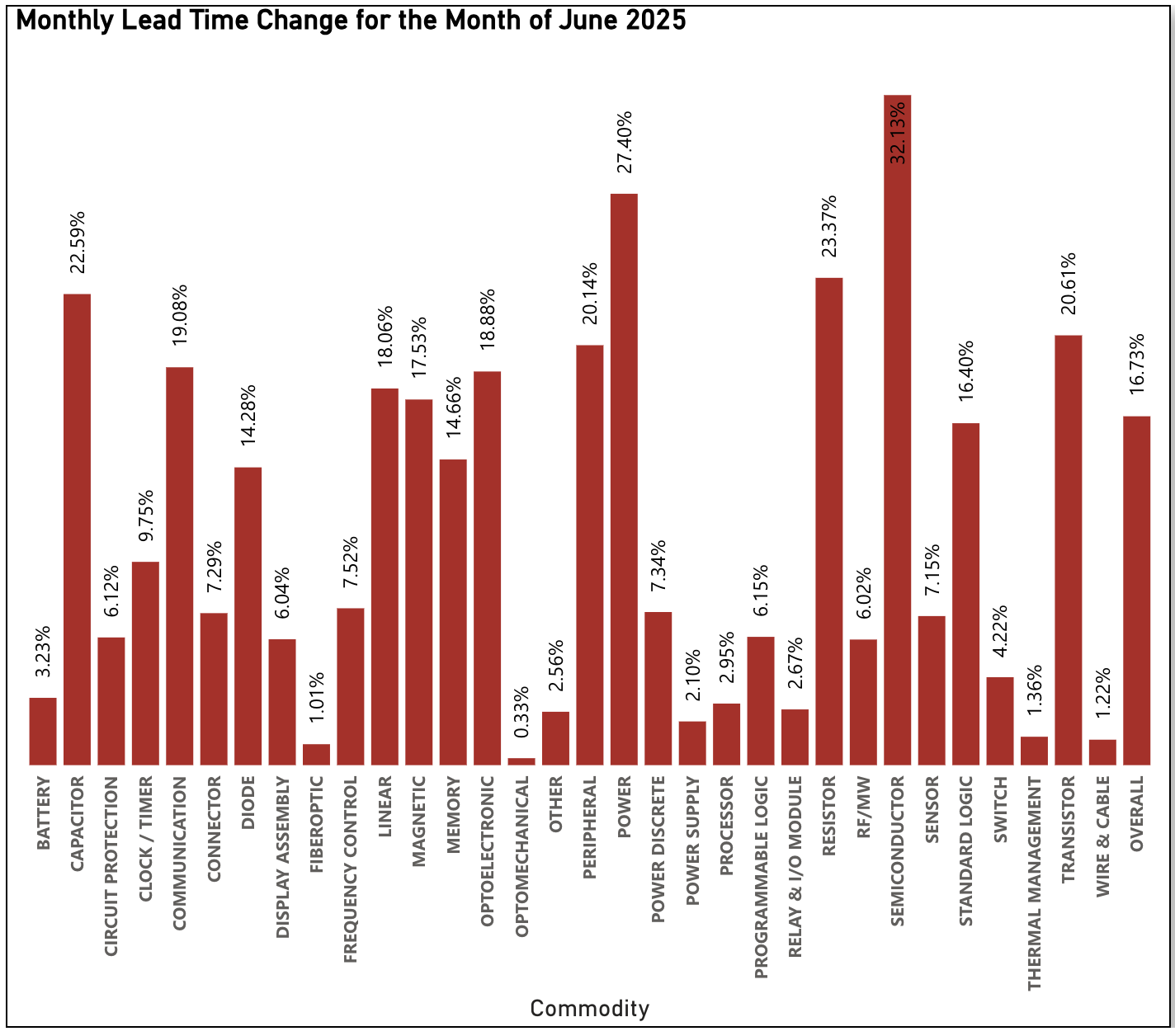

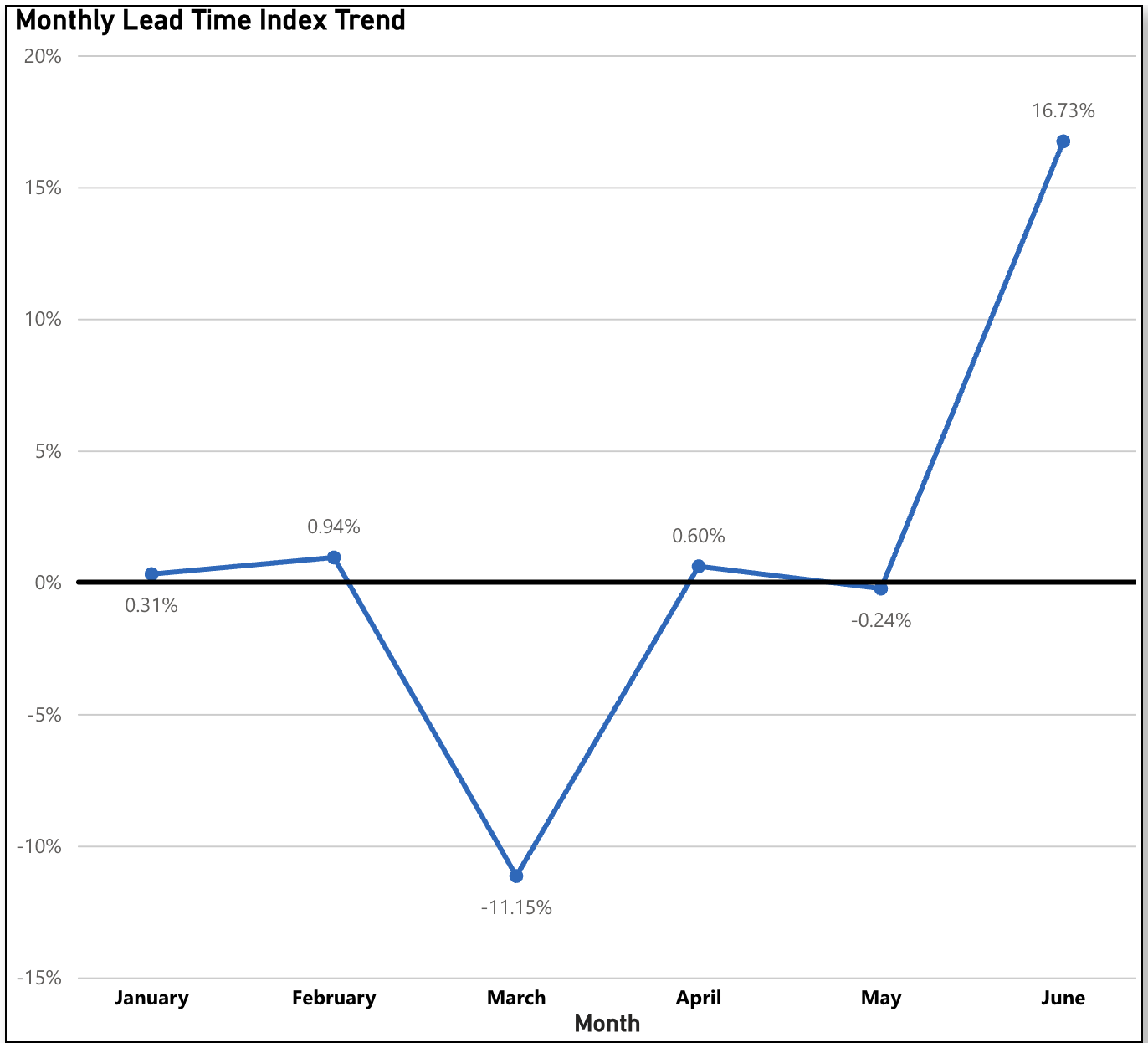

June Sees Largest Lead Time Increase of 2025

June recorded a sharp 16.73% increase in lead times, the largest jump since October 2024’s spike of 27.90%, and the second highest increase since reporting began. This significant shift signals a sudden bout of volatility following several months of relative lead time stability.

For the first time since reporting, every single commodity tracked saw an increase in lead times. The main contributors to this month’s large increase were Semiconductor (up 32.13% month-to-month), Power (up 27.40% month-to-month), Resistor (up 23.37% month-to-month), and Capacitor (up 22.59% month-to-month). Of the 32 tracked commodities, 13 saw a lead time increase of higher than 10%.

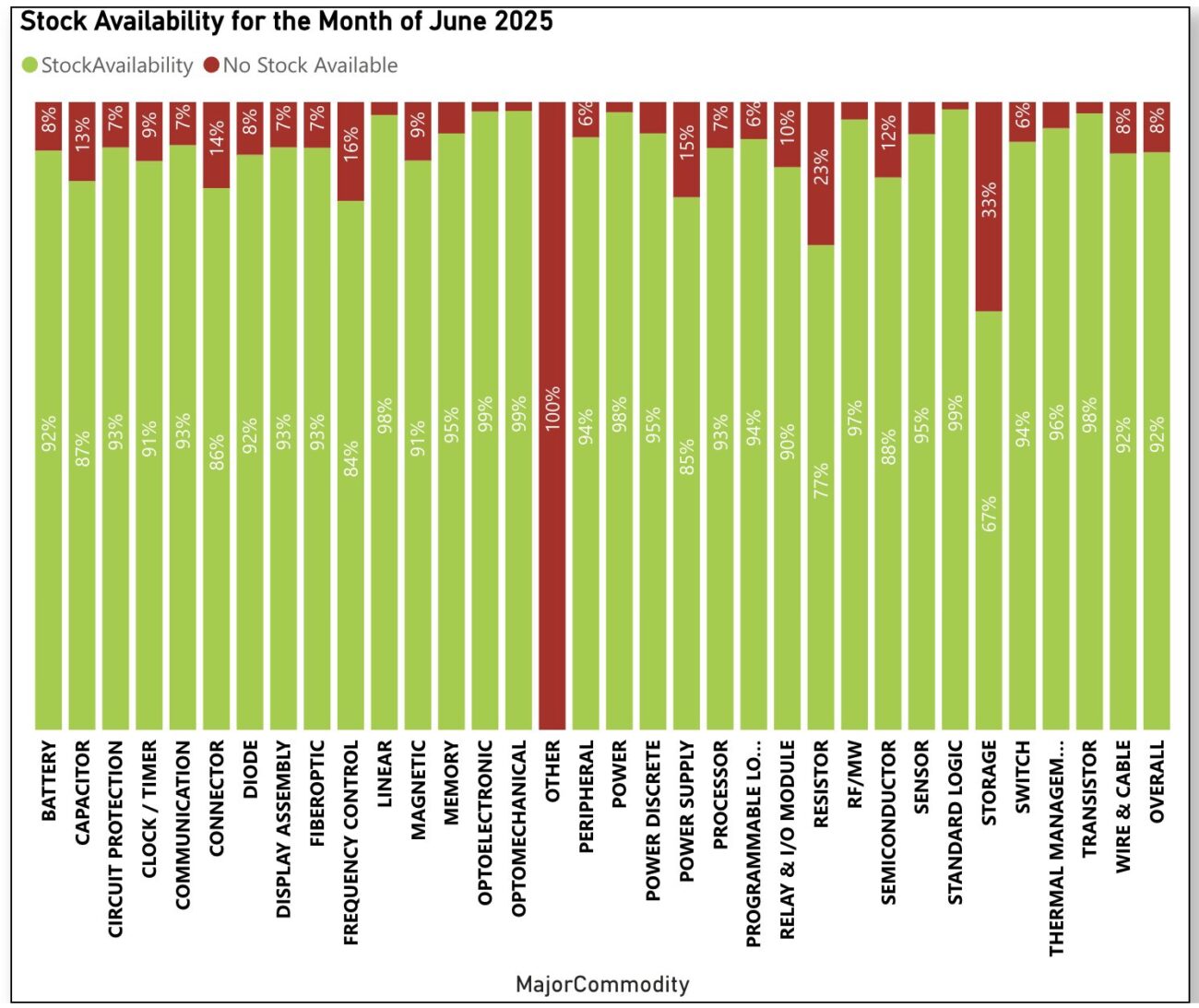

Stock Availability Remains Steady in June at 92%

For the third consecutive month in a row, stock availability has remained consistent at 92% available. This consistency continues the broader trend, suggesting that inventory positions remain healthy for buyers. Minimal changes were observed across the commodity categories compared to May, further reinforcing a stable supply environment. Those components leading the way from an availability perspective include Optoelectronic, Optomechanical and Standard Logic (all at 99% available), Linear, Power, and Transistor (at 98% available), and RF/MW (at 97% available). Those components pushing downward on this trend include Other (at 0% available), and Storage (at 67% available).

Sign up for our newsletter for more on the electronic components market.