Electronics Market Continues to Heat Up in December

Lytica is the world’s only provider of electronic component spend analytics and risk intelligence using actual customer data. As a result of our unique position in the marketplace, we’ve been able to work with 100+ customers across industries (including 20% of the Fortune 500) in analyzing over $425 billion in electronic component spend. We’ve curated up-to-date insights on the state of the electronic component market and will be sharing them with you each month.

Lytica’s component basket of goods used in our analysis is comprised of 15,800 electronic components across 22 categories, consisting of the most popular devices used by our customers. These indices are intended to show trends in the market. Individual component and BoM analysis is offered by Lytica as a service to our customers.

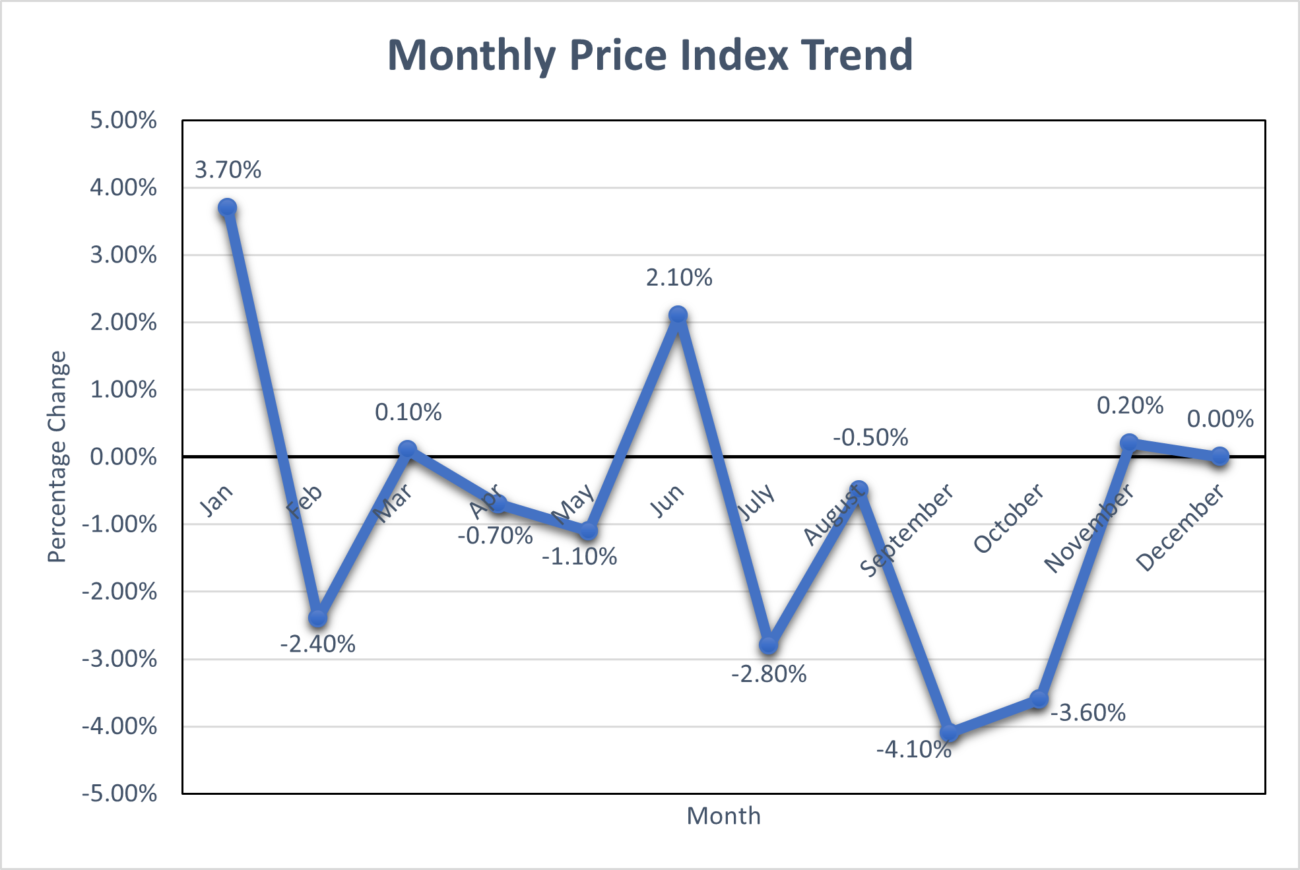

Electronic Component Pricing Remains Unchanged to End 2023

Electronic components pricing remained unchanged in December, following a slight 0.2% increase in November. December’s readout of electronics pricing marks the only month of 2023 where prices did not change. This also puts an end to the trend where one month of price increases was always followed by at least one or more months of price decreases. Ultimately, electronic pricing remains compelling for procurement teams.

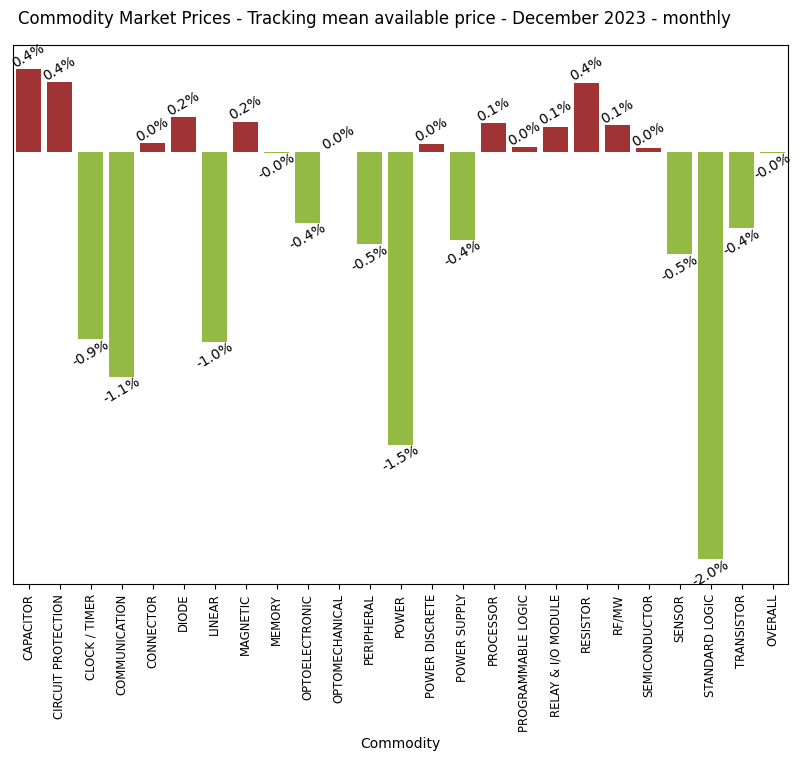

The biggest drivers in this pricing readout are the 6 different commodities with no change in price from November (Connector, Memory, Optomechanical, Power Discrete, Programmable Logic, and Semiconductor).

The commodities pushing downward against this trend include Standard Logic (down 2.0% Month-to-Month following a previous increase of 1.4% Month-to-Month), Power (down 1.5% Month-to-Month following a previous decrease of 0.2% Month-to-Month) and Communication (down 1.1% Month-to-Month following a previous decrease of 0.2% Month-to-Month), among others.

In terms of commodities pushing upwards against this trend, we saw price increases for Capacitor, Circuit Protection and Resistor components (up 0.4% Month-to-Month), and Diode and Magnetic components (up 0.2% Month-to-Month), among others.

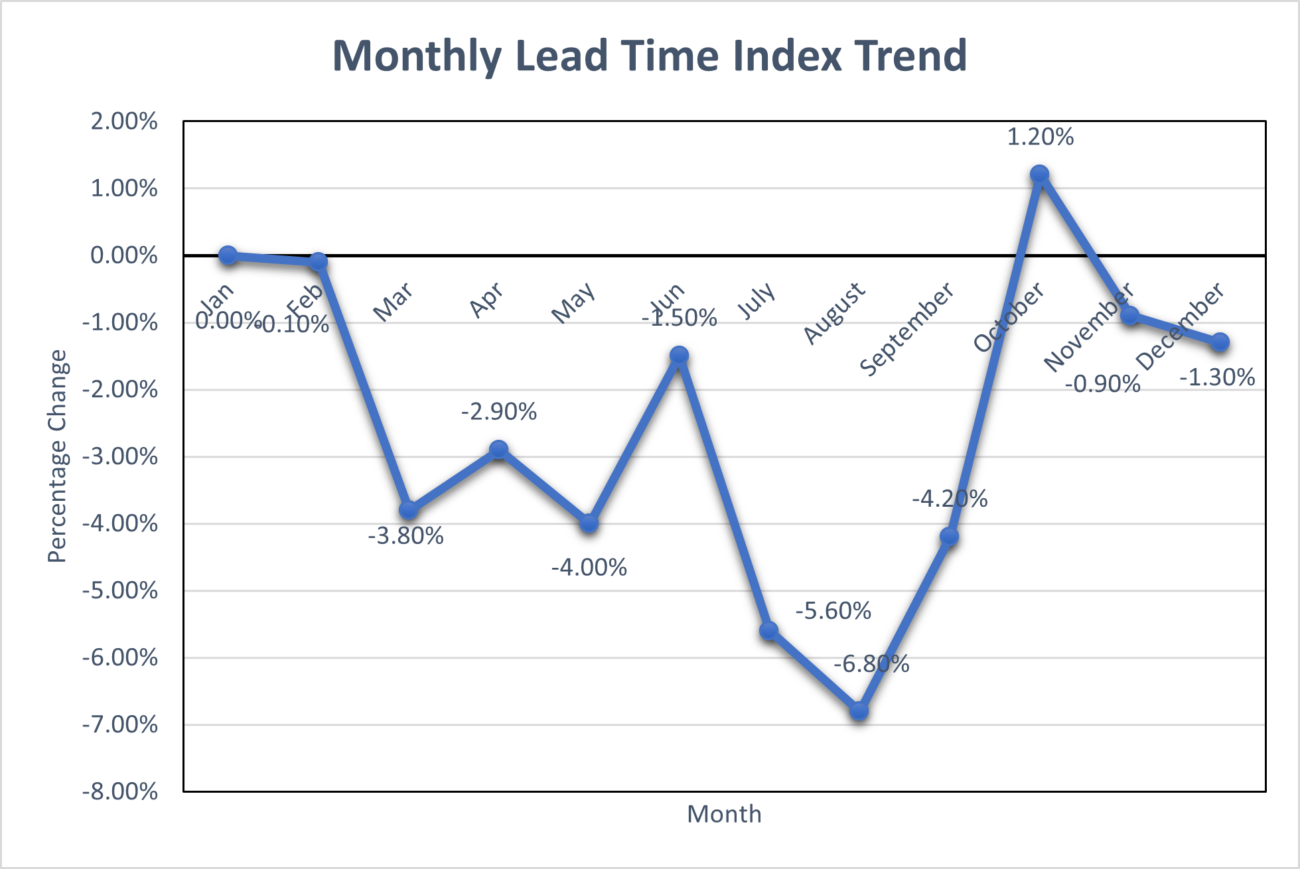

Electronic Component Lead Times Continue to Decrease in December

In December, we saw average overall lead times for electronic components tracked once again decrease by 1.3%. This maintains the pattern observed throughout 2023 of decreasing lead times for tracked components, with the only exception being in October.

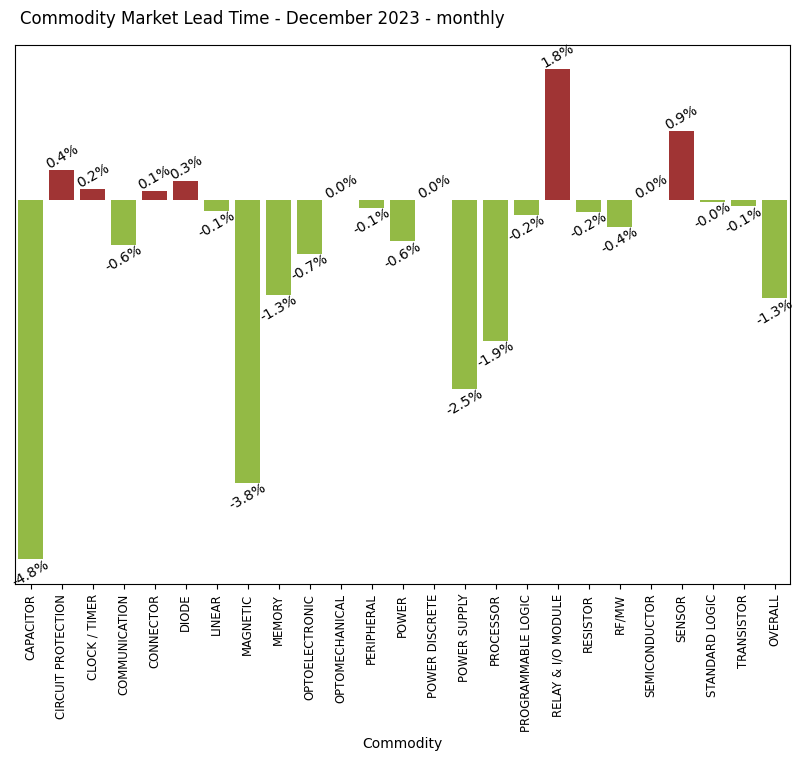

The decrease in lead times was driven largely by Capacitor (down 4.8% Month-to-Month), Magnetic components (down 3.8% Month-to-Month) and Power Supply (down 2.5% Month-to-Month). Those commodities pushing back on December’s trend included Relay & I/O Module components (up 1.8% Month-to-Month), Sensor (up 0.9% Month-to-Month), and Circuit Protection (up 0.4% Month-to-Month).

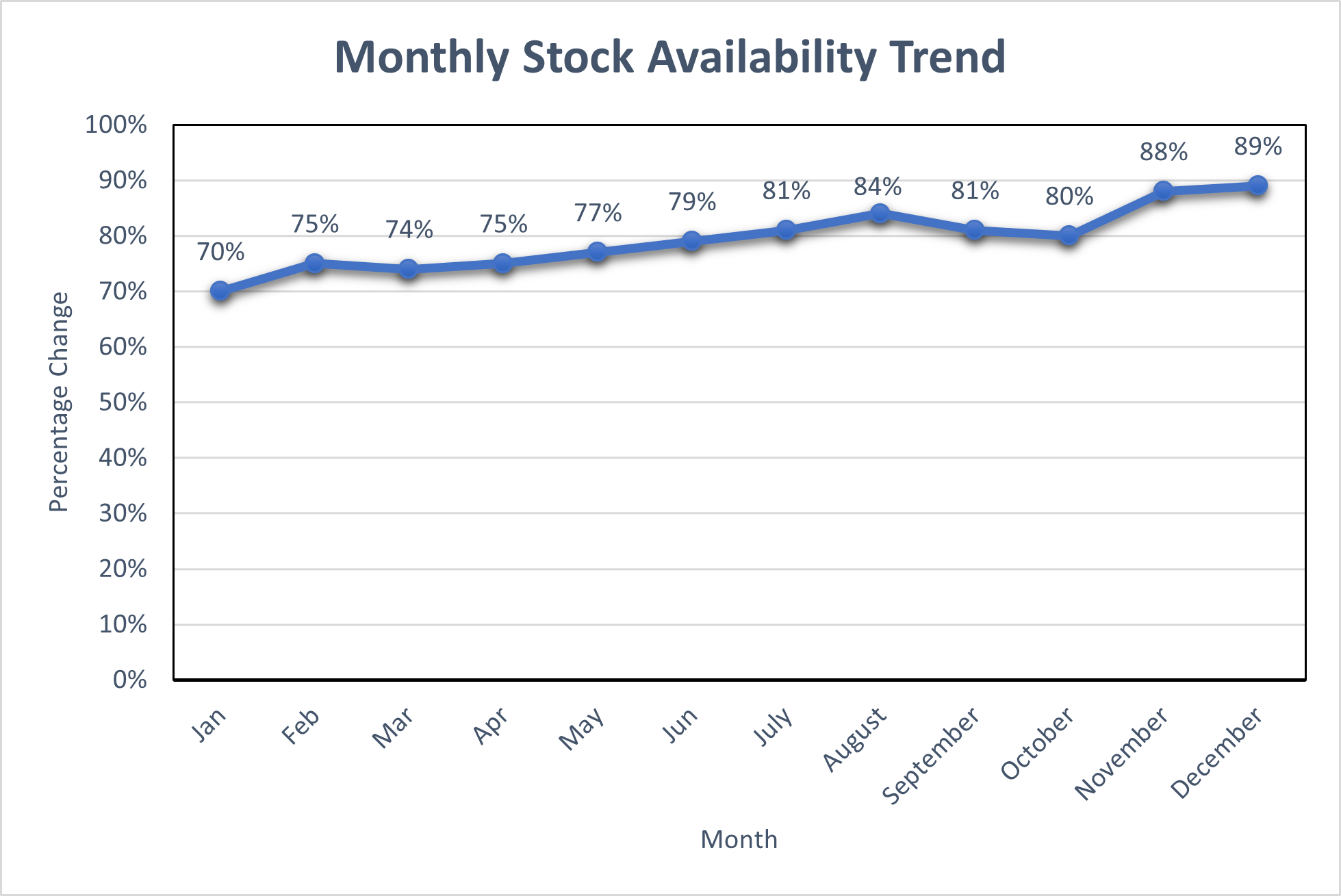

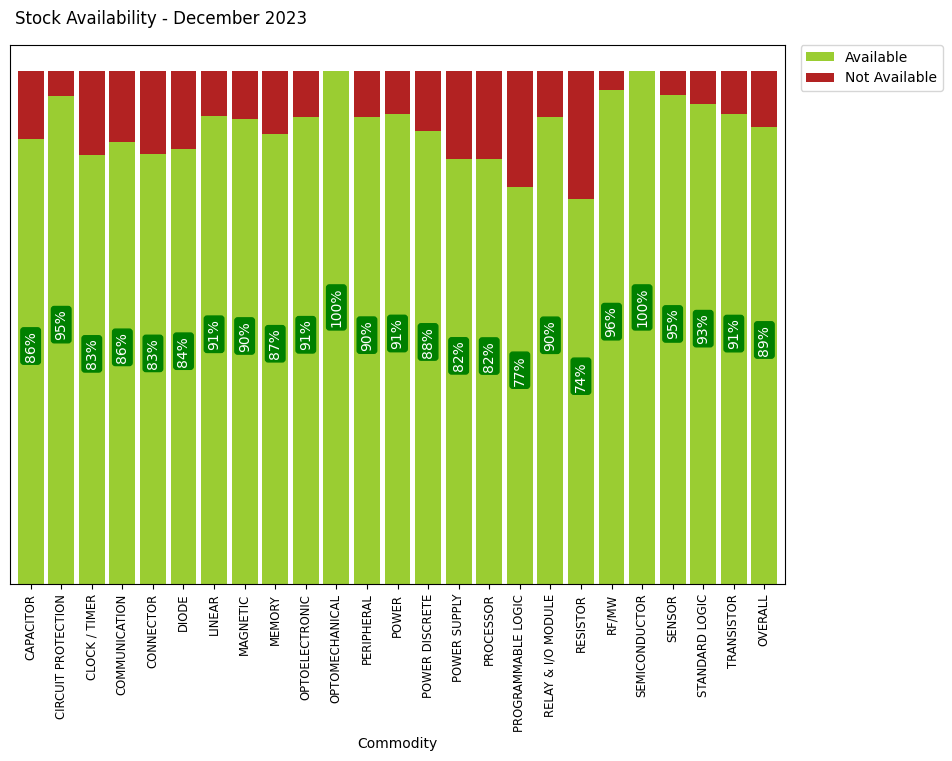

Electronic Component Availability Increases Once Again in December

In December, electronic component availability increased to 89% of all tracked electronic components available, up from 88% in October. Although a small increase, this continues the trend of increasing stock availability to end the year. Those components leading the way from an availability perspective in December included once again Optomechanical and Semiconductors (both 100% Available), RF/MW components (96% Available), and Circuit Protection (95% Available).

Sign up for our newsletter for more on the electronic components market. Make sure to also stay tuned for our 2023 State of the Electronic Component Market Round-Up coming soon!