State of the Electronic Components Market: February 2026

A Steady Headline Masks a Two-Speed Market Beneath the Surface

Lytica is the world’s only provider of electronic component spend analytics and risk intelligence using real customer data. As a result of our unique position in the marketplace, we’ve been able to work with 100+ customers in analyzing over $550 billion in electronics spend. We curate up-to-date insights on the state of the electronic component market and share them here with you each month. Subscribe today to receive these each month upon release.

Lytica’s component basket comprises 165,000 electronic components across more than 30 categories, including the most popular devices used by our customers. These indices are intended to show market trends. Individual component and BOM analysis is offered by Lytica as a service to our customers.

Stability on the Surface, Divergence Underneath

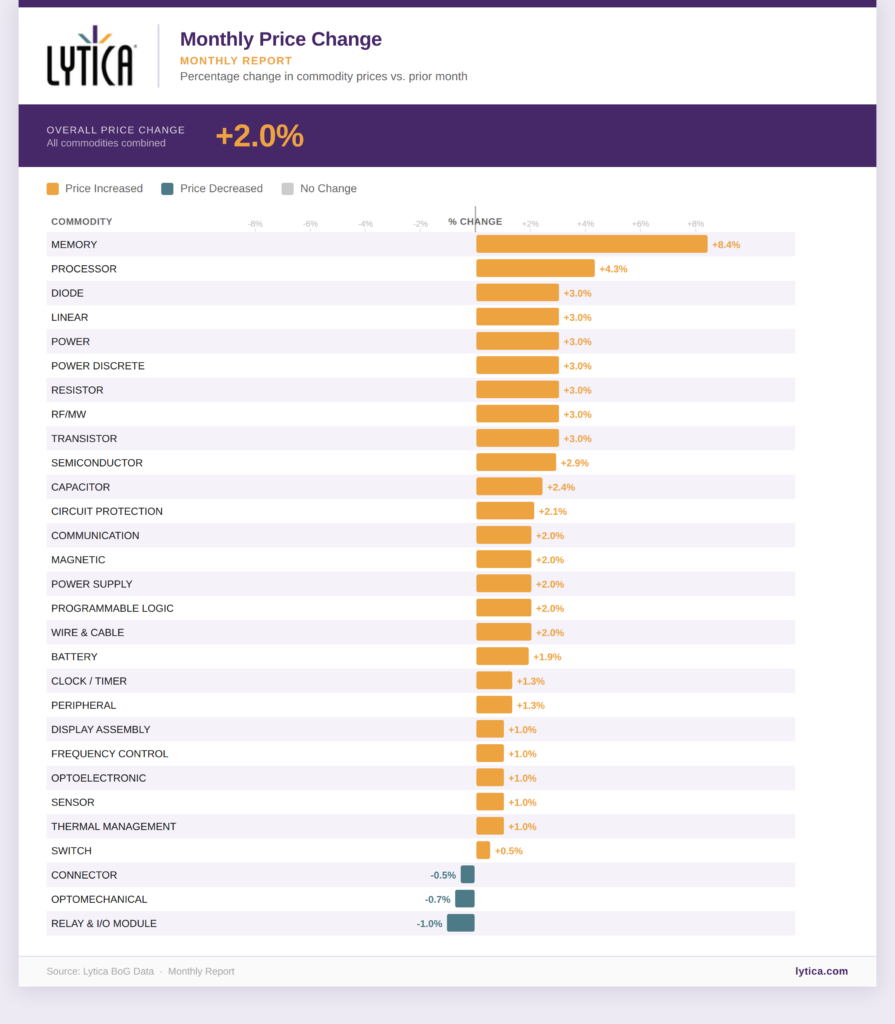

February’s overall price index came in at 2.00%, matching January’s reading. On the surface, that looks like a stable market. But the headline number is doing a lot of averaging, and the story of a two-speed electronics market became harder to ignore.

At one extreme, memory surged 8.40% and processors rose 4.30%, driven by AI and data center demand, and a broad cluster of semiconductor categories posted 3.00% increases. At the other end, three categories declined: Connectors (–0.50%), Optomechanical (0.70%), and Relay & I/O Modules (–1.00%). Procurement teams focused on memory-heavy or power-heavy BOMs are experiencing more inflation than the headline suggests.

Copper held above $12,900 per metric tonne on the London Metal Exchange, directly contributing to 2% price increases across wire and cable, magnetics, and power supply categories. Lithium carbonate rebounded sharply toward $24,000, sustaining upward pressure on battery pricing.

The monthly price index increased 3.47% month-over-month in December, extending the upward trajectory observed throughout the fourth quarter. Earlier softness gave way to a directional shift in recent months, with sustained increases leading into December. While price increases became more pronounced in specific categories, the broader market remained balanced, with movement driven by structural demand and upstream cost pressures rather than widespread supply disruption.

Monthly Price Change by Category

Memory (+8.40%)

Memory remained the dominant inflation driver in February. Manufacturers continue to shift capacity toward High Bandwidth Memory (HBM) and server DRAM, where margins are strongest, leaving standard memory segments increasingly undersupplied.

The 8.40% monthly increase captured in Lytica’s basket-level index understates what is happening in contract negotiations, where some product families are seeing prices double quarter-over-quarter. Memory is projected to represent roughly $200 billion of the semiconductor industry’s anticipated $1 trillion in 2026 sales. If these dynamics persist, memory inflation alone could begin pulling the overall index higher.

Processors were the second-largest mover in February, reflecting strong demand from computing and AI workloads. Advanced logic remains at the center of the AI infrastructure boom, with hyperscale customers pulling forward orders for data center and inference hardware.

Processor (+4.30%)

Processors were the second-largest mover in February, reflecting strong demand from computing and AI workloads. Advanced logic remains at the center of the AI infrastructure boom, with hyperscale customers pulling forward orders for data center and inference hardware.

Diode, Linear, Power, Power Discrete, Resistor, RF/MW, Transistor (+3.00%)

A broad cluster of seven categories posted 3.00% increases in February, forming the backbone of the market’s middle tier. Diode prices increased due to continued firmness in the discrete semiconductor market. Linear IC pricing rose as foundry cost pass-throughs and late-2025 list price adjustments continued working through the system. Taiwan Semiconductor Manufacturing Company (TSMC) reported price increases of 3–10% for sub-5nm offerings creating ripple effects across analog and mixed-signal segments.

Power and Power Discrete components continued their upward trend in February, with EV and industrial demand remaining primary drivers. China’s commitment to doubling EV charging capacity represents a sustained, policy-backed demand signal that flows directly through to component pricing. Silicon carbide (SiC) and gallium nitride (GaN) devices are strongly affected as they are the materials of choice for high-efficiency EV inverters and charging systems. For teams carrying these components on their BOM, the outlook is clear: this is structural demand, and pricing pressure is unlikely to ease in the near term. Resistors, RF/MW, and Transistors also posted gains this period, though the story there is simpler as it was steady end-market demand moving in line with the broader semiconductor pricing environment.

Geopolitical factors also shaped pricing in this cluster. The Nexperia situation where Dutch authorities intervened in the company’s Chinese operations, leading to halted wafer shipments and reduced production, continued to tighten supply for discrete components used heavily in automotive applications. While the acute disruption has eased, pricing has not fully normalized and lead times in some product families remain extended.

Semiconductor (+2.90%)

The broader Semiconductor category posted a 2.90% increase, just below the 3% discrete cluster. This reflects the weighted average across the semiconductor landscape, combining the strong upward pull from memory and processors with more moderate movement in categories like programmable logic and communication ICs. Wafer cost pass-throughs and early-year contract resets are the primary drivers.

Capacitor, Circuit Protection, Communication, Magnetic, Power Supply, Programmable Logic, Wire & Cable (+2.00% to +2.40%)

The broad mid-tier represents the largest group of categories, all posting increases in the roughly 2% range. Capacitor prices rose 2.40%, slightly above the group, reflecting continued demand and material cost pressures. Communication ICs rose due to general semiconductor pricing pressure and steady infrastructure demand. Circuit Protection increased 2.10% in line with broader discrete firmness. Programmable Logic rose 2.00% as semiconductor cost increases flowed through. Power Supply assemblies moved up as higher input costs flowed into finished products.

Copper is the common thread running through several categories in this tier. Magnetic components were directly influenced by elevated copper prices. Wire and Cable prices increased 2.00%, driven by copper price increases.

Battery (+1.90%)

Battery prices increased modestly this month as manufacturers continued passing through earlier lithium cost increases. Battery-grade lithium carbonate spot prices have risen to approximately $24,000 per metric tonne, up from under $11,000 a year earlier. The driver is clear: global energy storage installations hit 106 GW in 2025, a 43% year-on-year increase, according to Wood Mackenzie, with 2026 forecast to reach 359 GWh. Grid-scale storage and AI data center expansion are both fueling lithium demand, and neither is slowing down.

Lower-Tier Categories (+0.50% to +1.30%)

Several categories posted more modest increases in the 0.50–1.30% range: Clock/Timer and Peripheral at 1.30%, Display Assembly, Frequency Control, Optoelectronic, Sensor, and Thermal Management at 1.00%, and Switch at 0.50%. These categories generally represent more mature product lines where competitive pressure, depreciated manufacturing equipment, and ample multi-source availability are keeping price increases contained. Display Assembly at 1.00% reversed last month’s decline, suggesting the panel market may be stabilizing.

Declining Categories: Connector (–0.50%), Optomechanical (–0.70%), Relay & I/O Module (–1.00%)

Three categories posted price declines in February: Connector (–0.50%), Optomechanical (–0.70%), and Relay & I/O Module (–1.00%). While small, these are notable in a market where virtually every category increased in January. The Relay & I/O Module decline—the largest in the basket—may reflect softening demand in industrial automation segments or inventory normalization after earlier overbuild.

These decliners, along with the 0.50–1.30% lower tier, are the mathematical counterweight that keeps the overall index flat at 2.00% despite Memory’s 8.40% surge and the 3% semiconductor cluster. This is the clearest illustration of the two-speed market: AI-adjacent categories are inflating rapidly while mature categories are flat to declining, and the headline sits squarely between them.

Monthly Price Index Trend

Overall Index: +2.00% in February — Unchanged from January The overall monthly price index held at 2.00% for the second month in a row. That looks stable, but the average is hiding a growing gap between categories. Memory rose 8.40% while Relay & I/O Module fell 1.00% — same month, same index, completely different cost experience depending on your BOM.

The stability of the overall index through both January and February suggests the market has settled into a pattern where AI-driven inflation in high-demand segments is being offset, in aggregate, by softer pricing in more commoditized categories. Whether this equilibrium holds into Q2 depends largely on the trajectory of memory pricing.

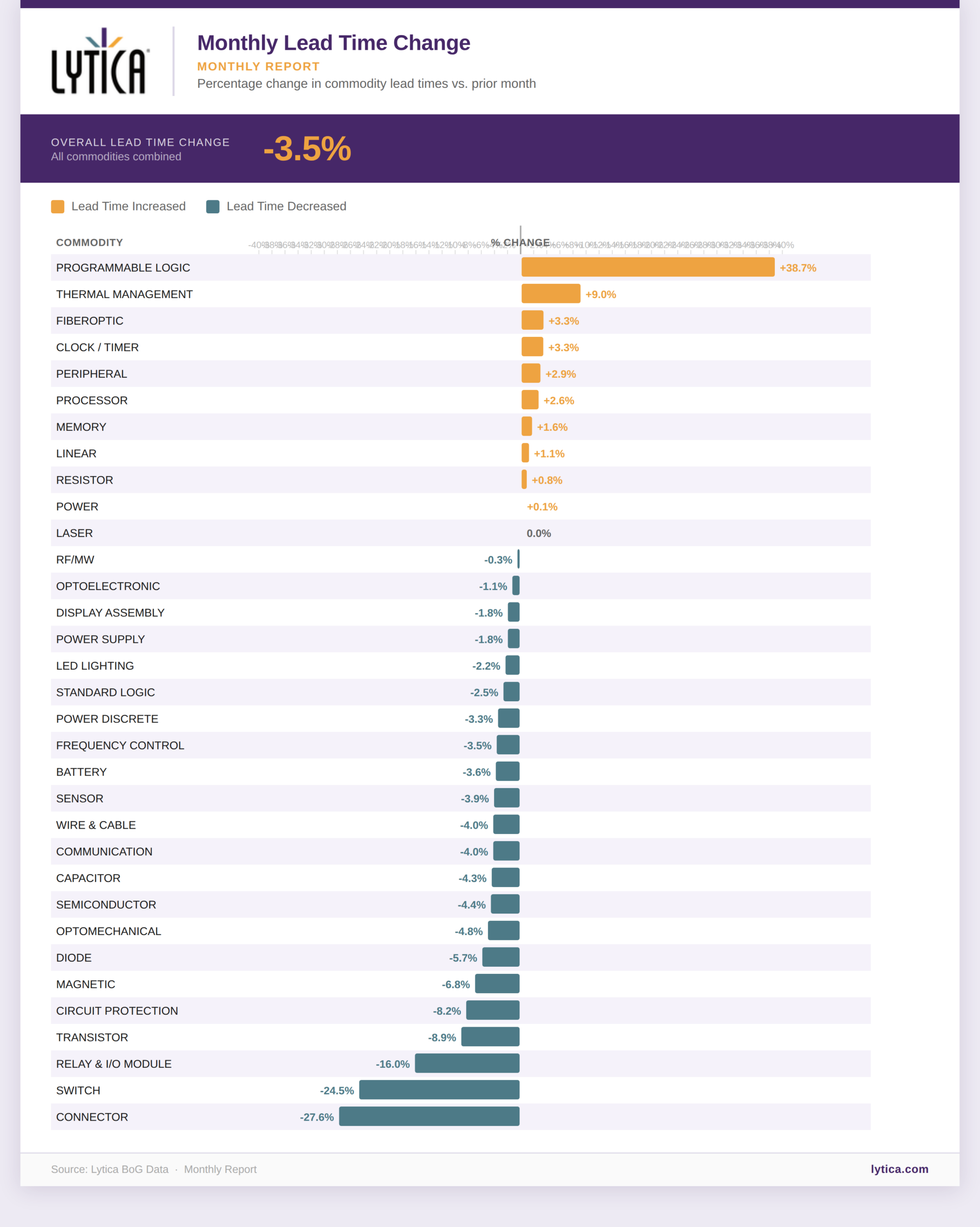

Lead times compressed significantly in February, with the overall lead time index falling to –3.53%—a sharp acceleration from January’s –0.90%. Most categories saw lead time reductions, with particularly notable improvements in Connector (–27.58%),

Monthly Lead Time Change

February saw a meaningful compression in lead times, as the overall lead time index declined by 3.53%, a notable acceleration compared with the 0.90% decrease recorded in January. Most categories posted shorter lead times during the month, suggesting improved availability across much of the component landscape. The strongest reductions were recorded in Connectors, down 27.58%, followed by Switches, down 24.50%, Relays and I/O Modules, down 15.99%, Transistors, down 8.90%, and Circuit Protection, down 8.15%.

Ten categories saw lead times extend. Programmable Logic spiked 38.68%—by far the largest increase—suggesting a tightening of supply that has not yet fully translated into pricing (the category posted only a 2.00% price increase). Thermal Management (+8.99%), Fiberoptic (+3.33%), Clock/Timer (+3.30%), Peripheral (+2.88%), and Processor (+2.59%) also saw increases, while Memory (+1.59%), Linear (+1.12%), Resistor (+0.78%), and Power (+0.05%) posted marginal extensions.

Lead Time Index Trend

Lead Time Index: −3.53% in February — Accelerating from January’s −0.90%

Lead times compressed nearly four times faster in February than in January. This is a positive signal: supply chains are loosening across most categories even as prices continue to rise. The combination points to a market driven by cost pass-through and supplier repricing, not by shortages.

The broad-based compression is significant. Of the 33 tracked categories, 22 saw lead times shorten — led by Connector (−27.58%), Switch (−24.50%), and Relay & I/O Module (−15.99%). The exceptions are worth watching: Programmable Logic lead times spiked 38.68%, the largest increase in the basket, suggesting demand is outstripping supply in a way that hasn’t fully shown up in its modest 2.00% price increase yet. Thermal Management (+8.99%) and Processor (+2.59%) also extended, both consistent with the demand pressure visible in their pricing data..

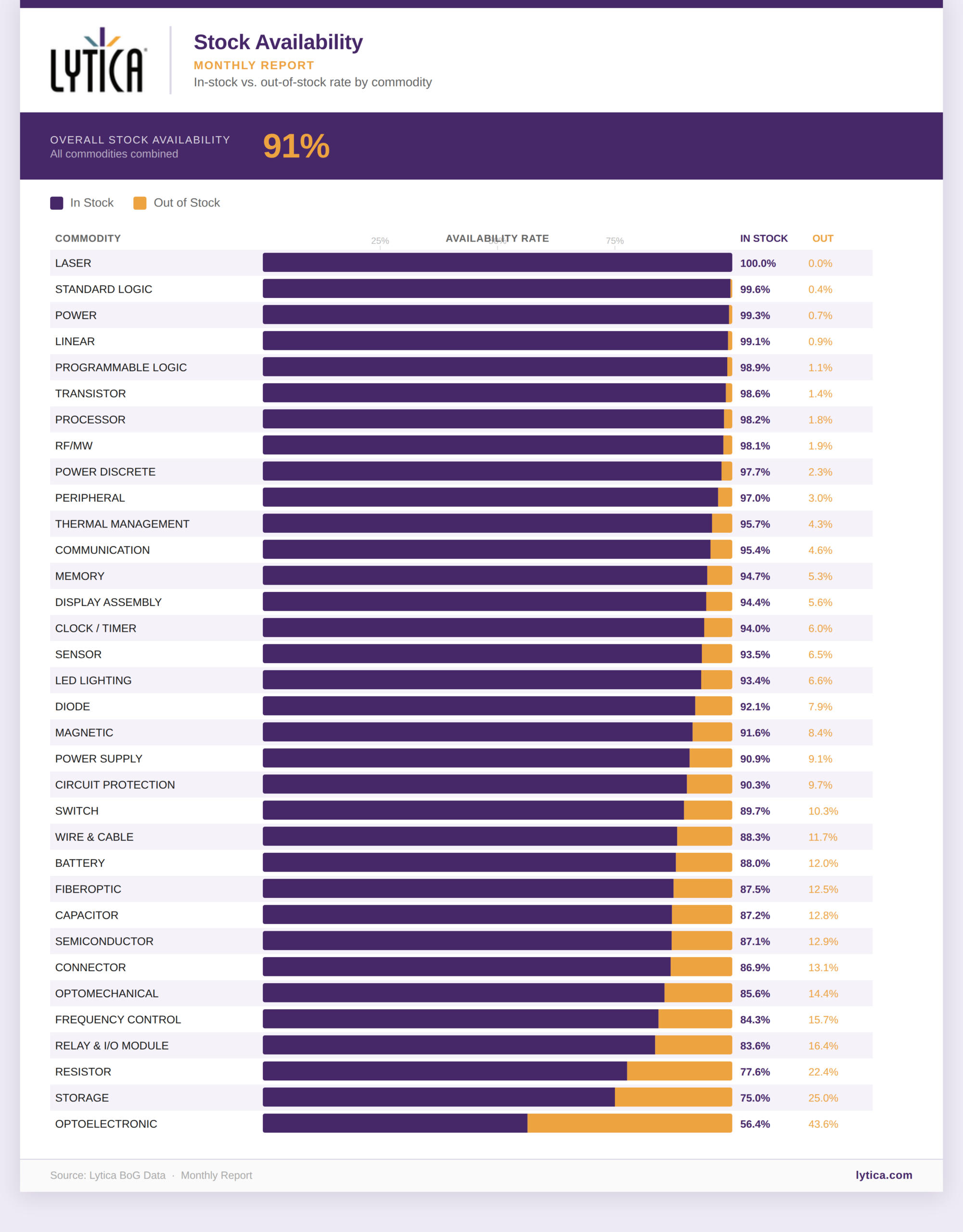

Stock Availability

The table below shows in-stock rates by category. Many categories are above 90%, with active semiconductor categories like Linear (99.1%), Power (99.3%), and Programmable Logic (98.9%) showing particularly healthy availability. Memory at 94.7% is notable—despite being the market’s strongest inflation driver at +8.40%, stock levels remain relatively high, reinforcing the interpretation that memory price increases are driven by supplier repricing and capacity reallocation rather than outright shortages.

A few categories stand out on the low end. Optoelectronic availability dropped to just 56.4%—the lowest in the basket by a wide margin—suggesting genuine supply constraints in that segment. Storage (75.0%) and Resistor (77.6%) also show tighter availability, though neither posted price declines, indicating that lower stock levels are being absorbed by the market without acute disruption. Relay & I/O Module availability at 83.6% aligns with its –1.00% price decline, suggesting a segment where softening demand rather than tight supply is the dominant dynamic.

Looking Ahead

Key takeaways for procurement teams

The forces behind the current market divergence are mutually reinforcing and unlikely to resolve in the near term. AI infrastructure investment shows no signs of slowing, wafer and fab cost increases are still working through contracts.

For procurement teams, the key takeaway is that the aggregate 2% index obscures more than it reveals. BOM-level analysis is now essential: the 9.4 percentage-point spread from Memory to Relay & I/O Module means that two companies in the same industry can face radically different cost pressures depending on their component mix. Granular, category-level monitoring should replace reliance on headline benchmarks.

Looking forward to the next few months, the memory market is the variable most likely to shift the overall index. If DRAM and NAND contract prices continue their historic trajectory, the weight of memory and semiconductor inflation will eventually overwhelm the deflationary offset from mature categories. Early qualification of alternates, diversification across geographies and channels, and active monitoring of tariff developments will be essential through the remainder of the year.

Sources and References

The following sources were consulted in preparing this report to provide broader market context, pricing data, and geopolitical analysis, alongside Lytica’s proprietary component basket data.

All About Industries, “Semiconductor Market 2026: AI Drives Growth, Regulation Slows Europe,” March 2026. https://www.all-about-industries.com/semiconductor-market-2026

Carbon Credits, “Lithium Prices Climb Again in 2026,” March 2026. https://carboncredits.com/lithium-prices-climb-again-in-2026-sending-stocks-skyward-nili/

Counterpoint Research, “Memory Prices Surge Up to 90% From Q4 2025,” February 5, 2026. https://counterpointresearch.com/en/insights/Memory-Prices-Surge-Up-to-90-From-Q4-2025

Deloitte Insights, “2026 Semiconductor Industry Outlook,” February 11, 2026. https://www.deloitte.com/us/en/insights/industry/technology/technology-media-telecom-outlooks/semiconductor-industry-outlook.html

Forex.com, “Trade to watch 2026: Copper’s time to shine?” February 3, 2026. https://www.forex.com/en-us/news-and-analysis/trade-to-watch-2026-copper-s-time-to-shine/

SIA via Tom’s Hardware, “Semiconductor industry on track to hit $1 trillion in sales in 2026,” February 6, 2026. https://www.tomshardware.com/tech-industry/semiconductors/semiconductor-industry-on-track-to-hit-usd1-trillion-in-sales-in-2026

SoftwareSeni, “DRAM Prices in 2026 Have Doubled,” March 2026. https://www.softwareseni.com/dram-prices-in-2026-have-doubled-and-the-numbers-are-getting-worse/

Sourceability, “2026 Semiconductor Industry Outlook + M&A,” 2026. https://sourceability.com/post/semiconductor-industry-outlook-for-2026-shows-rebound-amid-mergers

Sourceability, “2026 Semiconductor Industry Market Outlook,” 2026. https://sourceability.com/post/whats-ahead-in-2026-for-the-semiconductor-industry

StartUs Insights, “Semiconductor Industry Outlook 2026: Snapshot,” February 9, 2026. https://www.startus-insights.com/innovators-guide/semiconductor-industry-outlook-key-insights/

TechInsights, “McClean Report February 2026: Q1 Semiconductor Market Forecast Update,” February 2026. https://www.techinsights.com/blog/mcclean-report-february-2026-q1-semiconductor-market-forecast-update

The Register, “DRAM prices expected to nearly double in Q1,” February 2, 2026. https://www.theregister.com/2026/02/02/dram_prices_expected_to_double/

Tom’s Hardware, “Spiralling memory spot prices could trigger ‘industry cycle collapse,'” March 2026. https://www.tomshardware.com/tech-industry/memory-spot-prices-climbed-again-in-february

Trading Economics, “Copper — Price — Chart — Historical Data,” February 2026. https://tradingeconomics.com/commodity/copper

Trading Economics, “Lithium — Price — Chart — Historical Data,” February 2026. https://tradingeconomics.com/commodity/lithium

TrendForce, “Memory Price Outlook for 1Q26 Sharply Upgraded,” February 2, 2026. https://www.trendforce.com/presscenter/news/20260202-12911.html

WCCFTech, “Memory & NAND Prices Surged Over 90% In Q1 2026,” February 9, 2026. https://wccftech.com/memory-nand-prices-surged-90-percent-in-q1-2026/

Wood Mackenzie, “Global energy storage market surpasses 100 GW annual installation milestone in 2025,” January 2026. https://www.woodmac.com/news/opinion/global-energy-storage-market-surpasses-100-gw-annual-installation-milestone-in-2025/

Sign up for our newsletter for more on the electronic components market.