State of the Electronic Components Market: January 2026

2026 Begins with Supply Stability and Rising Prices

Lytica is the world’s only provider of electronic component spend analytics and risk intelligence using real customer data. As a result of our unique position in the marketplace, we’ve been able to work with 100+ customers in analyzing over $550 billion in electronics spend. We’ve curated up-to-date insights on the state of the electronic component market and will be sharing them with you each month.

Lytica’s component basket comprises 165,000 electronic components across more than 30 categories, including the most popular devices used by our customers. These indices are intended to show market trends. Individual component and BOM analysis is offered by Lytica as a service to our customers.

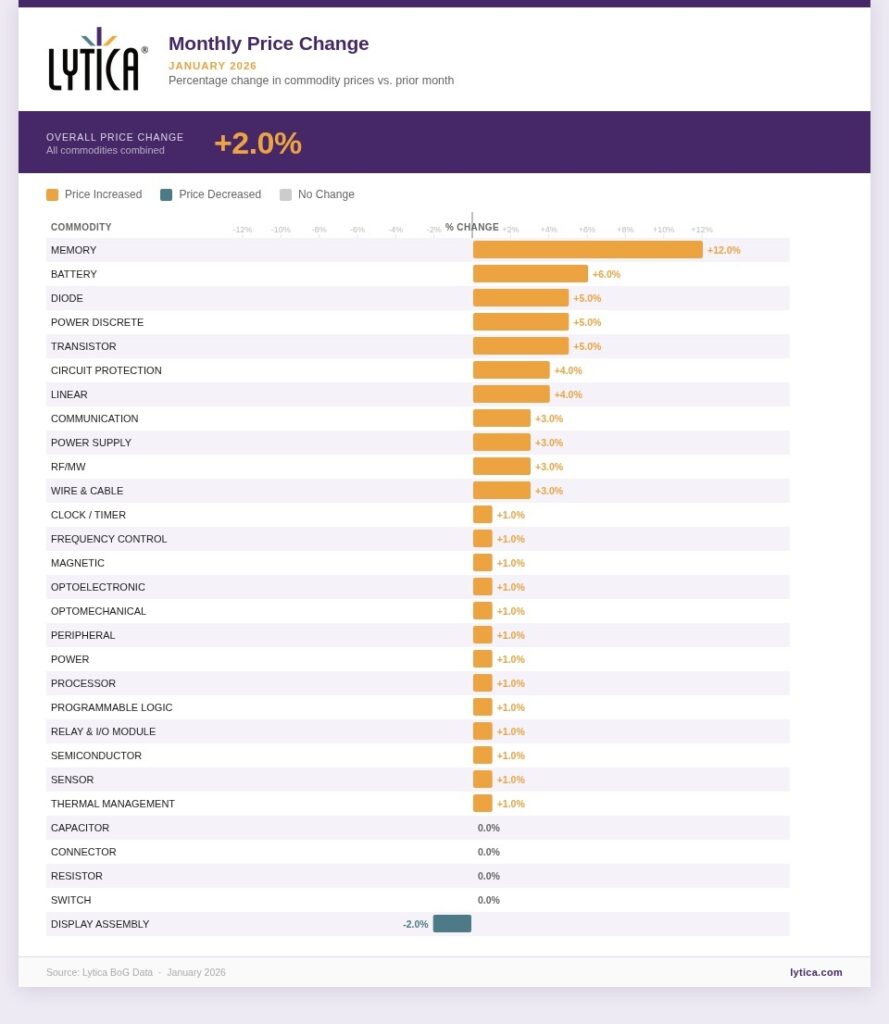

The start of 2026 shows semiconductor inflation that remains measured but steady, driven primarily by memory prices. Across the electronics supply chain, costs are hardening, not due to widespread shortages, but rather structural price adjustments and the typical commercial repricing that accompanies the new year.

Memory is the standout category in January as prices increased significantly. Other semiconductor segments are trending upward more quietly, as wafer costs filter through the chain and suppliers reset contract terms. Copper and lithium remain elevated but appear more stable than they were in late 2025. Display panels continue to soften, while passive components and electromechanical categories look comparatively steady.

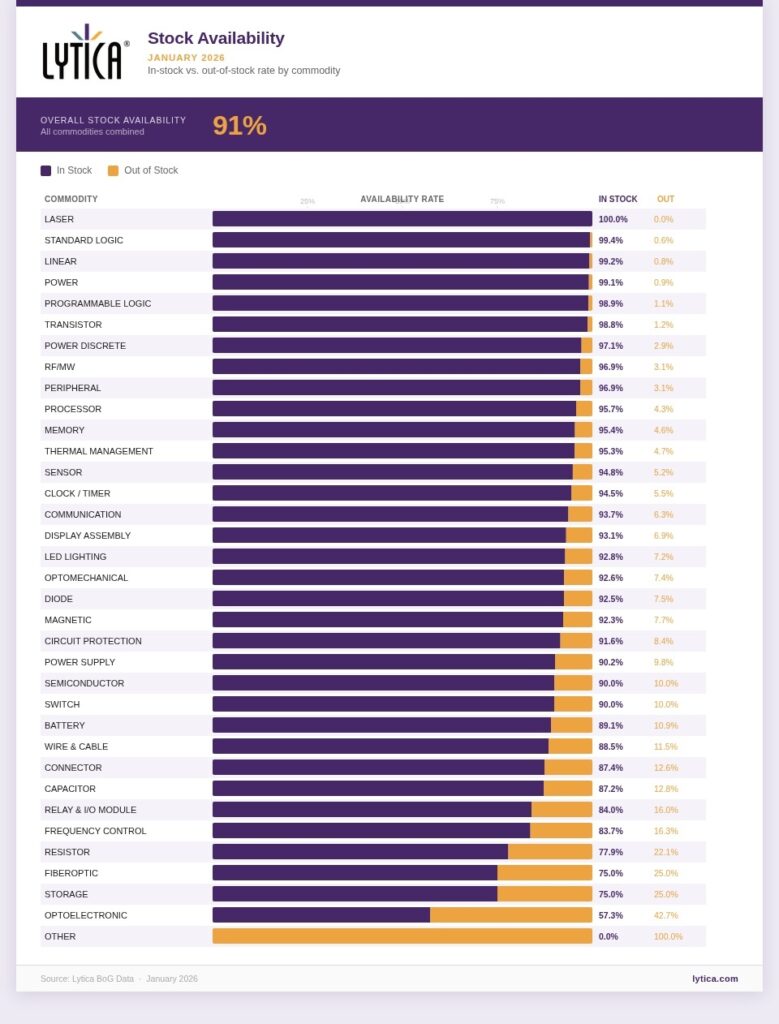

Lead times and stock availability help set the tone of the market. Availability is improving, and inventory coverage is generally healthy, yet prices continue to rise in key categories.

Broad Price Increases Across Electronics Components

The AI-driven super cycle that’s been reshaping this market for the past two years shows no signs of losing momentum, and manufacturers are responding accordingly — shifting capacity toward High Bandwidth Memory and server DRAM, where margins are stronger, and demand from AI hardware makers remains relentless. Standard memory availability is tightening as a result. Overall, memory prices rose 12% in January.

Battery pricing increased as elevated lithium carbonate and electrolyte costs carried into January contracts. Although lithium markets have stabilized compared to prior spikes, raw material input costs remain high. Strong energy storage demand continues to support firm pricing.

Power Discrete components (MOSFETs and IGBTs) were up roughly 5%. They continue to experience residual supply tightness, particularly in automotive and industrial segments. Although the acute shortages of prior years have eased, qualification timelines and EV demand continue to limit rapid supply flexibility. Elevated wafer pricing and Q1 contract resets further contributed to price firming. The increase reflects structural supply discipline rather than panic buying.

Linear and Analog ICs rose more than 4%, with Circuit Protection, Diodes, and Transistors up somewhere in the 4–5% range. No acute shortage is driving it — foundry cost pass-throughs and late-2025 list price adjustments working their way through the system account for most of the movement.

Across the broader landscape, increases were moderate but widespread, with copper and semiconductor input costs the common thread. Power Modules came in around 4%, where wafer pricing and historically high copper prices gave suppliers leverage at the negotiating table. Standard Logic, RF, and Communication ICs rose about 3% as suppliers realigned pricing with higher fab costs, though demand looks stable rather than overheated.

Power Supply Assemblies moved up roughly 3% as well; competitive pressure in finished goods kept the increases from going further. PCBs were up about 4% — copper and energy costs remain elevated even as the volatility from late 2025 has calmed, and fabricators are still passing the higher baseline through. Wire and Cable followed at around 3%, as copper stays structurally high despite the recent spike cooling off.

Display Assembly costs were an exception, falling around 2%, pushed down by manufacturing lines that have matured and production equipment that’s largely been depreciated out.

Monthly Lead Time Change

Lead times broadly compressed in January, with declines across many categories indicating that earlier bottlenecks continue to unwind. A few pockets moved the other way—small increases that look more product-specific than systemic. The key point is the backdrop: lead time improvement alongside rising prices suggests a market driven more by commercial resets and cost pass-through than by scarcity.

Stock Availability: A Positive to Start 2026

Stock availability remained strong across most major commodity groups in January, with high in-stock rates seen in many categories. This supports the view that rising prices reflect cost carryover and supplier re-pricing rather than supply shortages.

Market Interpretation

January’s signal is a little counterintuitive. Availability is improving, inventory is there and yet prices are climbing across multiple semiconductor categories, and the most plausible explanation isn’t a shortage story but structural repricing.

AI-driven demand has concentrated buying power in memory, pulling supplier attention and capacity with it. Wafer cost increases from late 2025 are now showing up in contracts. Copper and lithium keep input costs elevated on the materials side. And Q1 is simply when suppliers reset commercial agreements, giving them a natural window to protect margins, shortage or not.

Sign up for our newsletter for more on the electronic components market.