Electronics Market: Changing Lead Times, the Big Story for May

Lytica is the world’s only provider of electronic component spend analytics and risk intelligence using real customer data. As a result of our unique position in the marketplace, we’ve been able to work with 100+ customers in analyzing over $450 billion in electronics spend. We’ve curated up-to-date insights on the state of the electronic component market and will be sharing them with you each month.

Lytica’s basket of goods used in our analysis is comprised of 15,800 electronic components across more than 30 categories, consisting of the most popular devices used by our customers. These indices are intended to show trends in the market. Individual component and BoM analysis is offered by Lytica as a service to our customers.

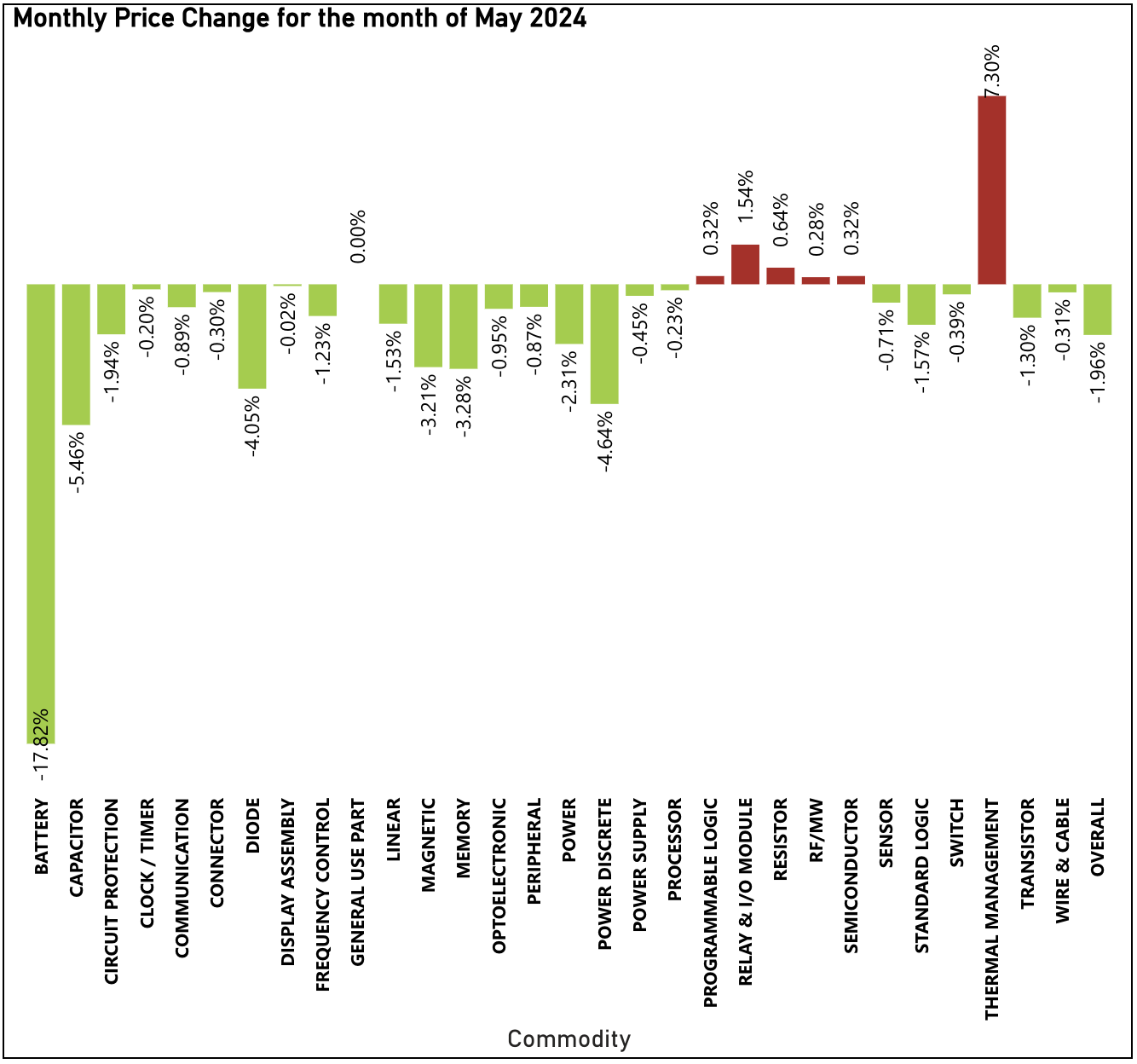

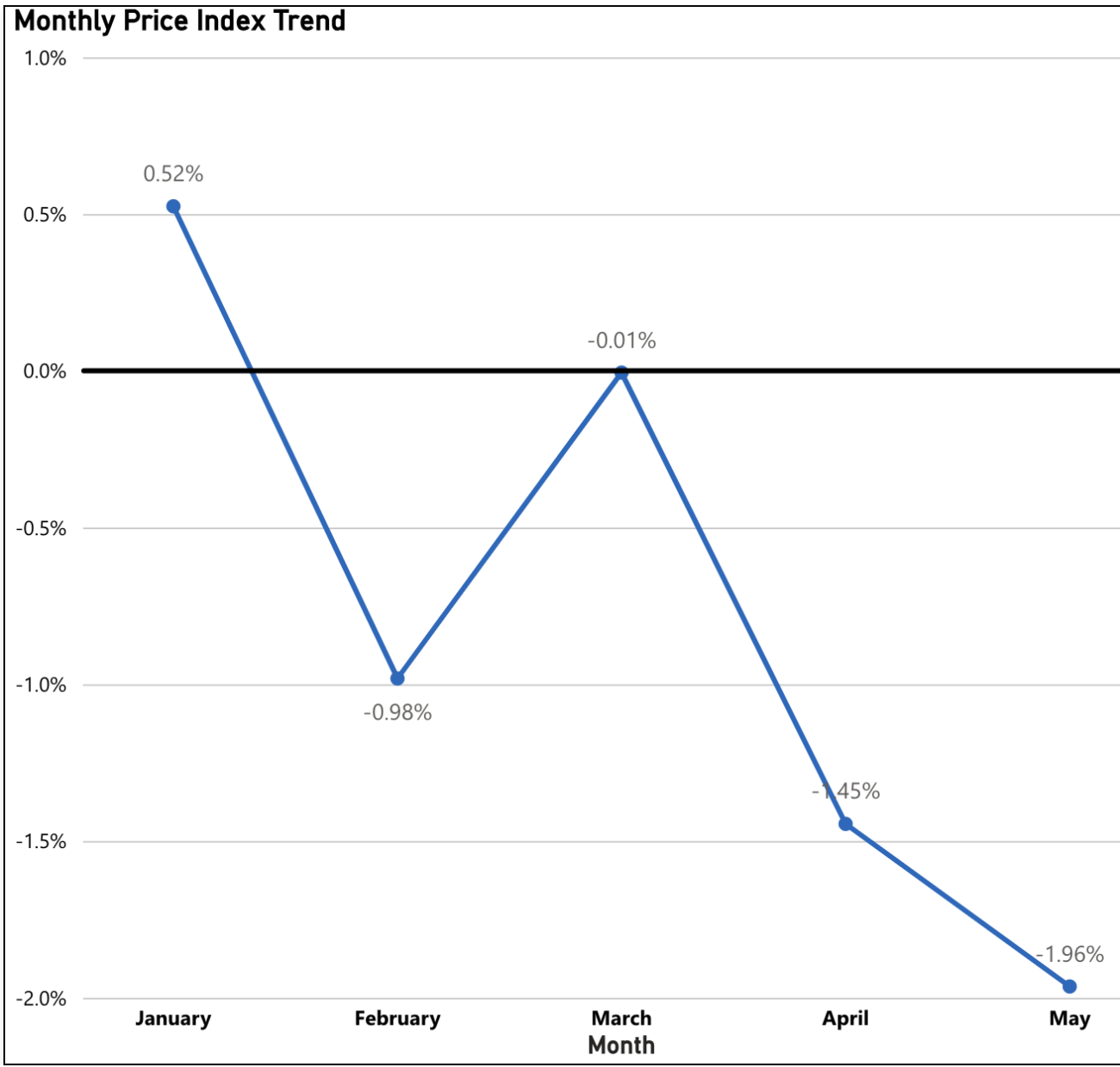

Electronic Component Pricing Sees Fourth Straight Month of Decreases in May

May sees the fourth straight month of pricing decreases in 2024, with an overall decrease of 1.96%. This pricing trend continues to be favorable for buyers, but the size of decreases seems to be stabilizing when compared to the large fluctuations seen throughout 2023.

The biggest drivers in this pricing readout include Battery (down 17.82% Month-to-Month, following a 0.69% increase in April), Capacitor (down 5.46% Month-to-Month), Power Discrete (down 4.64% Month-to-Month), and Diode (down 4.05% Month-to-Month).

The commodities pushing upward against this trend include Thermal Management (up 7.30% Month-to-Month following a decrease of 2.04% in April), Relay & I/O Module (up 1.54% Month-to-Month following a previous increase of 0.64% Month-to-Month) and Resistor (up 0.64% Month-to-Month) among others.

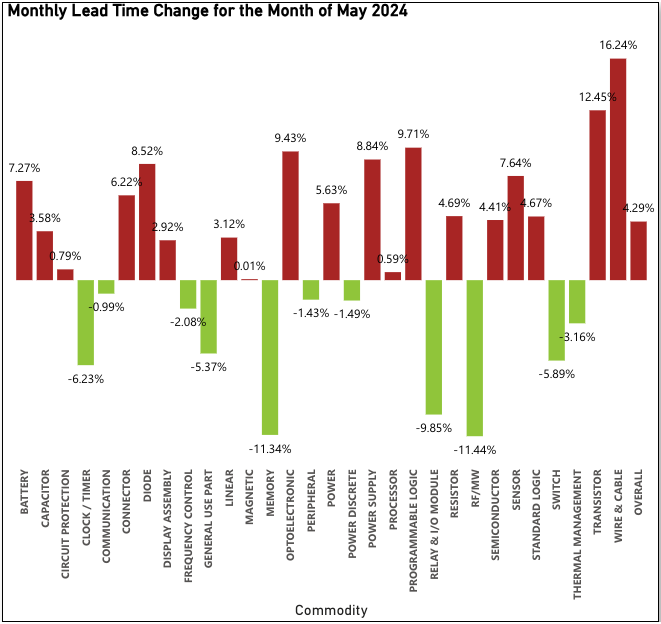

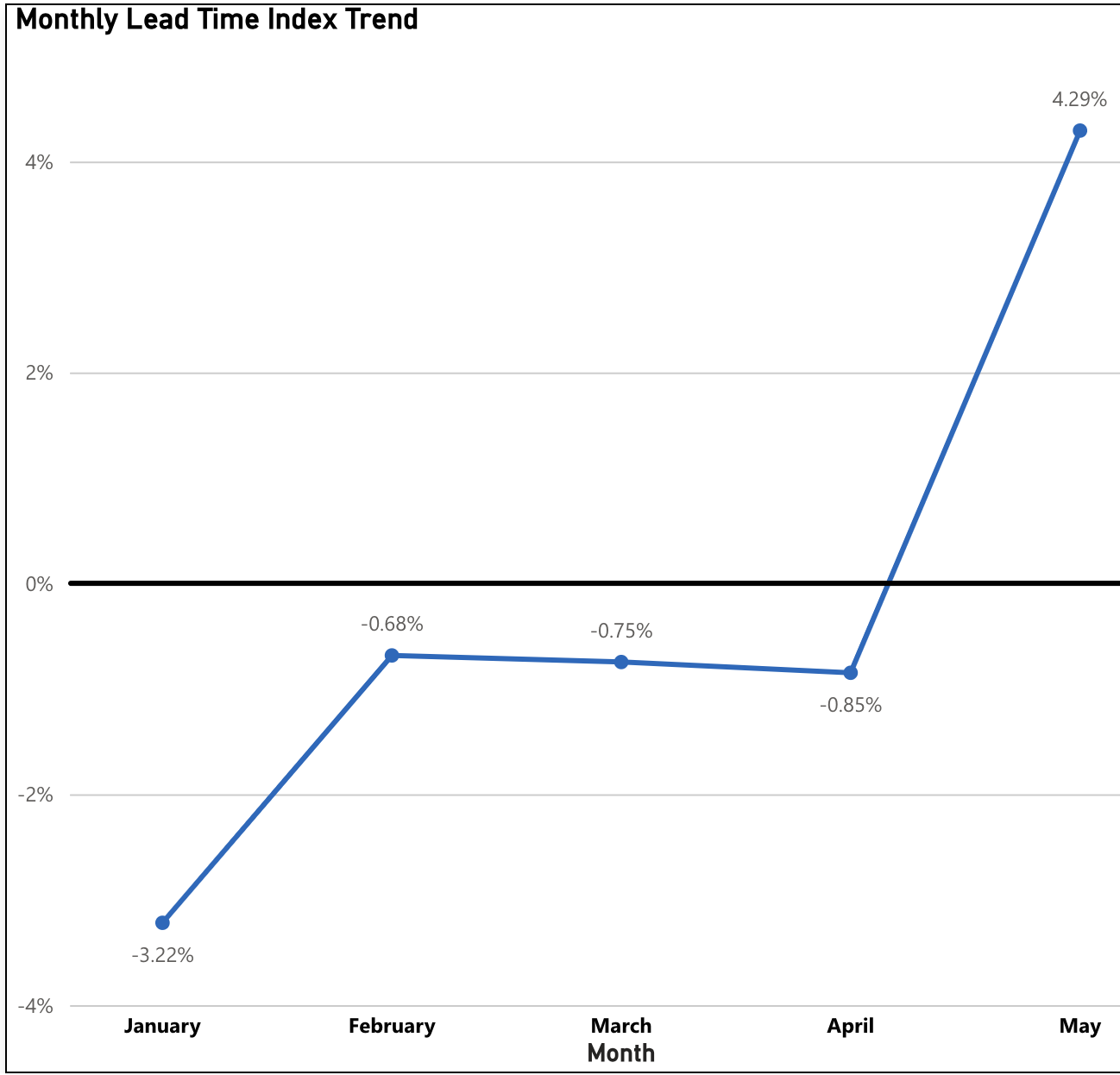

Lead Time Increases in May for the First Time Since October 2023

The trend of decreasing lead times in 2024 comes to an end in May, with an average lead time increase of 4.29% Month-to-Month. This marks the first increase since October 2023, and only the second increase in the past 17 months. This adds more evidence to last month’s report that the minimal lead time changes seen previously in 2024 could be an indication of stabilization in the market.

In May, 19 of the 30 tracked commodities (or 63%) saw an increase in lead times. The biggest drivers in this increase were Wire & Cable (up 16.24% Month-to-Month), Transistor (up 12.45% Month-to-Month), Programmable Logic (up 9.71% Month-to-Month), and Optoelectronic (up 9.43% Month-to-Month) among others.

Those commodities pushing back on Mays trend included RF/MW (down 11.44% Month-to-Month), Memory (down 11.34% Month-to-Month), Relay & I/O Module (down 9.85% Month-to-Month), and Clock/Timer (down 6.23% Month-to-Month), among others.

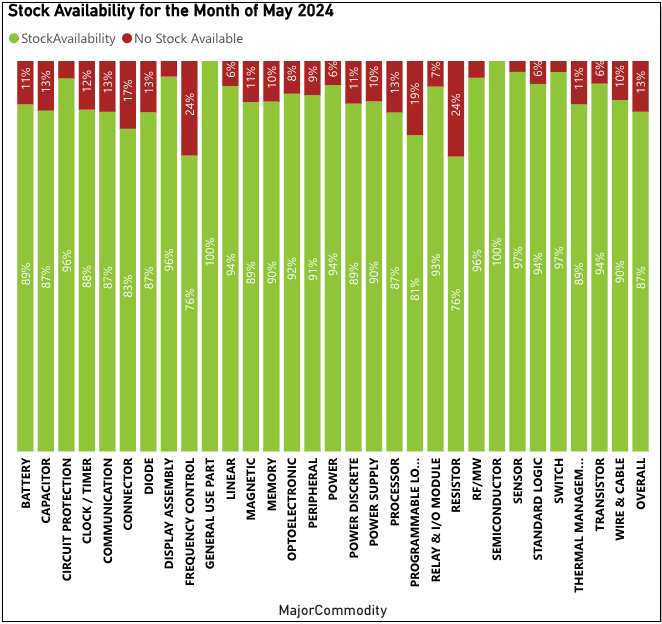

Electronic Component Availability Dips Back to 87% in May

In May, there was a slight decline in electronic component availability, marking the first dip in two months as it dropped to 87% of tracked components being available. This decrease came after consecutive months of record-high availability, with April and March both seeing levels at 90%. Despite this change, the overall trend remains positive for buyers, as 2024 has yet to fall below an 87% stock availability threshold. Those components leading the way from an availability perspective in May included Semiconductor and General Use Parts (both at 100% available), Sensor (at 97% available) and Circuit Protection, Display Assembly, and RF/MW (all at 96% Available).

Sign up for our newsletter for more on the electronic components market.