Electronics Market Is Offering Mixed Signals

Lytica is the world’s only provider of electronic component spend analytics and risk intelligence using actual customer data. As a result of our unique position in the marketplace, we’ve been able to work with 100+ customers across industries (including 20% of the Fortune 500) in analyzing over $425 billion in electronic component spend. We’ve curated up-to-date insights on the state of the electronic component market and will be sharing them with you each month.

Lytica’s component basket of goods used in our analysis is comprised of 15,800 electronic components across 22 categories, consisting of the most popular devices used by our customers. These indices are intended to show trends in the market. Individual component and BoM analysis is offered by Lytica as a service to our customers.

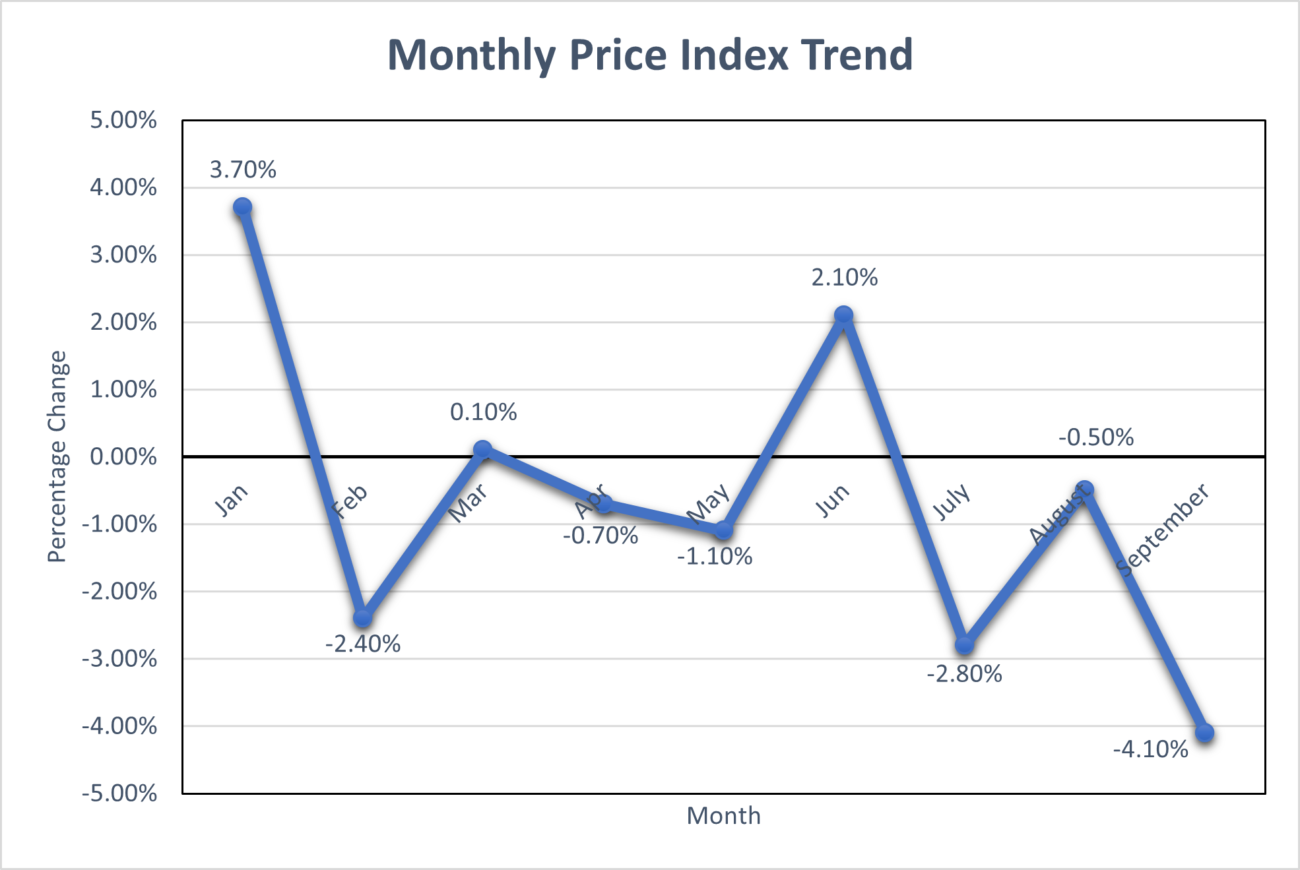

Electronic Component Pricing Declines Accelerate

Electronic component pricing fell again in September by 4.1% on average, following a monthly decline in August of just 0.5%, demonstrating accelerating pricing declines. As we mentioned in our last readout, electronic component pricing declines have been a common trend in the electronics market, as we’ve seen monthly price declines in 6 of the past 9 months.

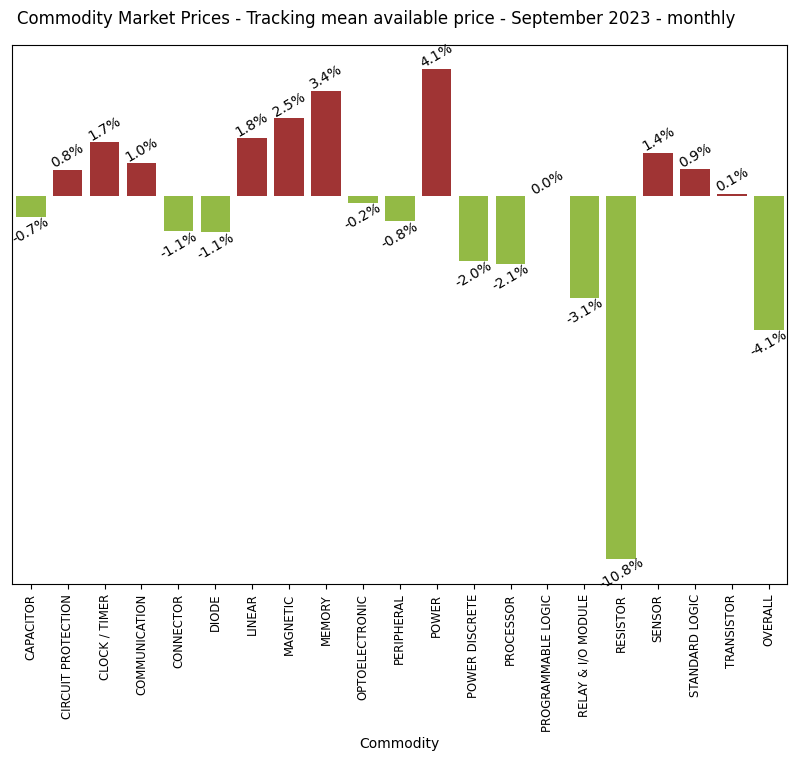

The biggest drivers in this pricing readout are Resistors (down 10.8% Month-to–Month following a previous decline of 3.7% Month-to-Month), Relay & I/O Modules (down 3.1% Month-to-Month) and Processors (down 2.1% Month-to-Month following a previous decline of 2.5% Month-to-Month).

In terms of commodities pushing against this trend, we saw prices rise for Power components (up 4.1% Month-to-Month), Memory components (up 3.4% Month-to-Month), and Magnetic components (up 2.5% Month-to-Month following a previous increase of 6.0% Month-to-Month).

Ultimately, September was another good month for electronics procurement teams to capitalize on falling electronic component pricing. Moreover, we can start to see some commodity trends forming over the past couple of months as a result of this readout.

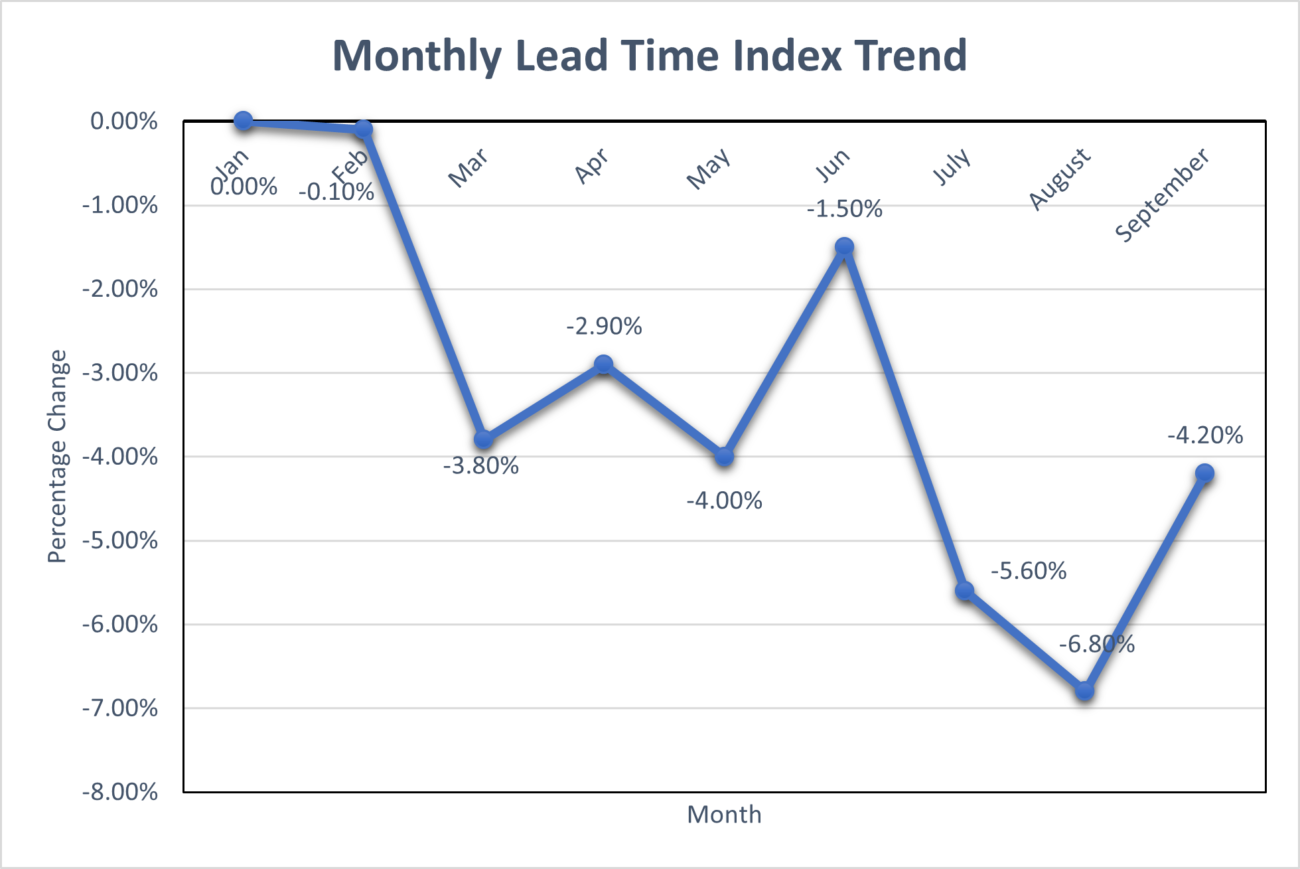

Electronic Component Lead Times Are Dropping But At A Slower Rate

In September, we saw average overall lead times for electronic components tracked improve by 4.2%, another Month-to-Month improvement but not as dramatic as we saw in August, which showcased lead times falling by 6.8% Month-to-Month on average.

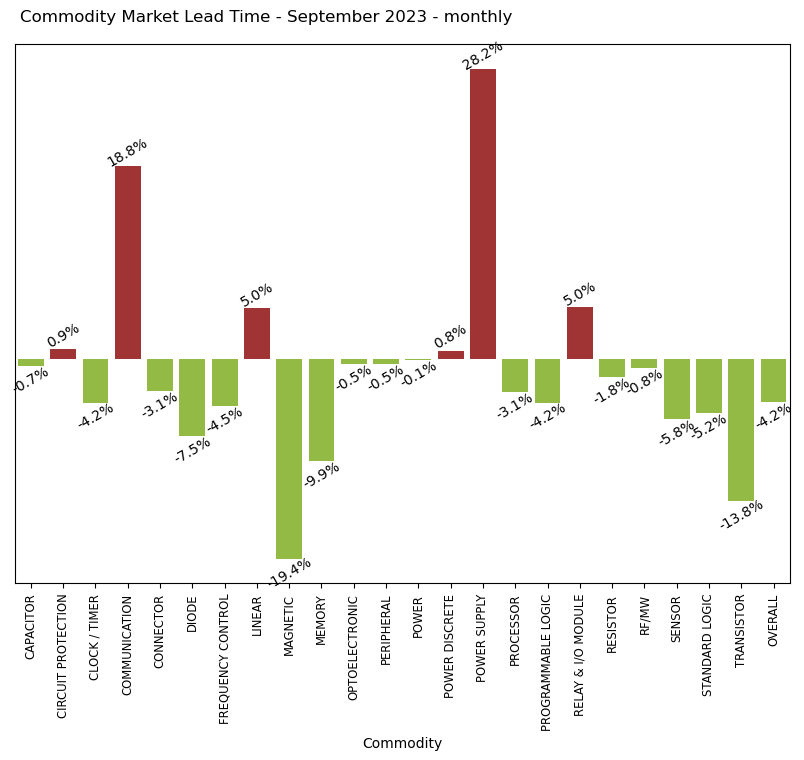

This drop in lead times were driven by Magnetic components (down 19.4% Month-to-Month following a previous decline of 35.5% Month-to-Month) and Transistors (down 13.8% following a previous decline of 25.3% Month-to-Month), and Memory (down 9.9% Month-to-Month). Those commodities pushing back on September’s trend included Power Supply components (up 28.2% Month-to-Month) and Communication components (up 18.8% Month-to-Month).

September’s readout continues the trend of lead times improving every month in 2023 thus far.

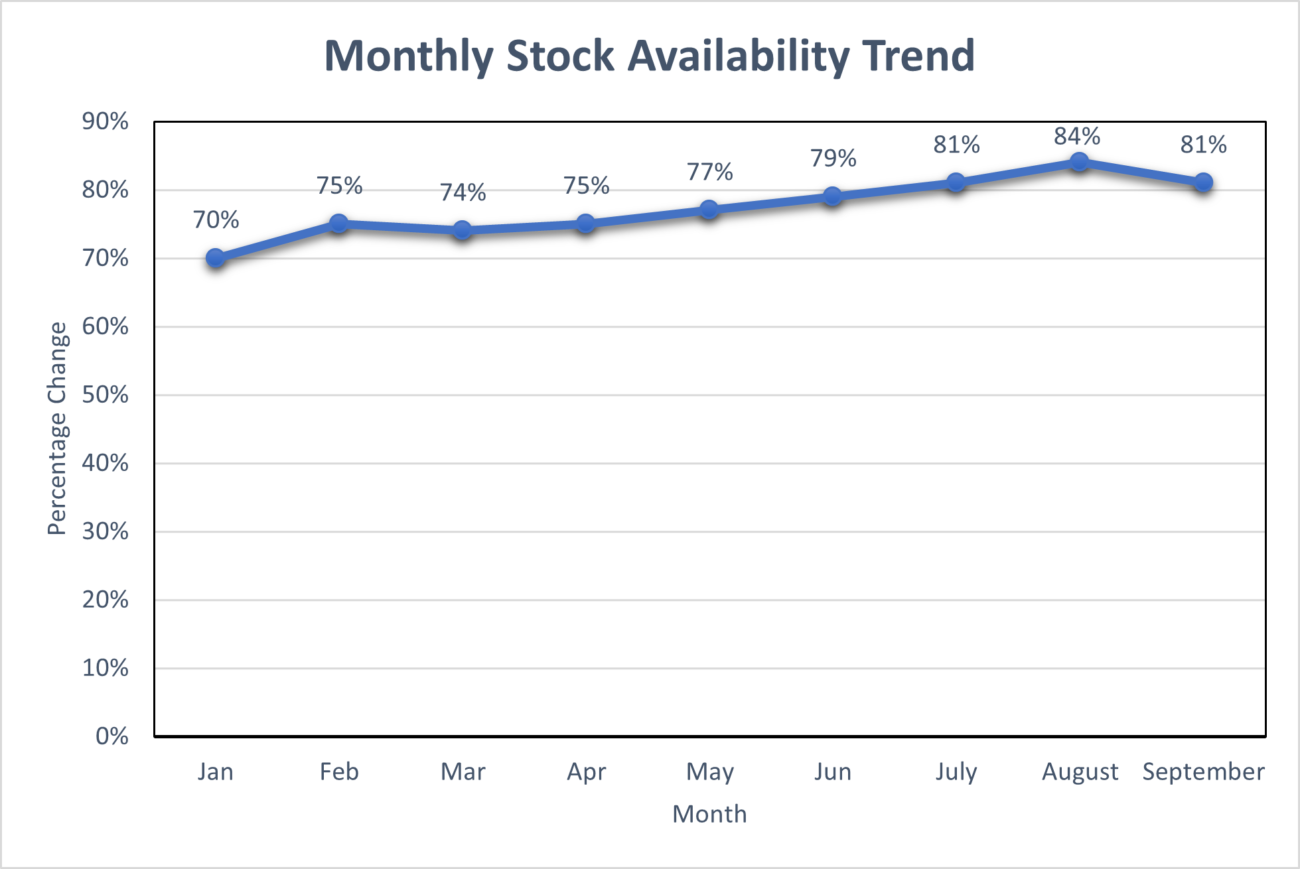

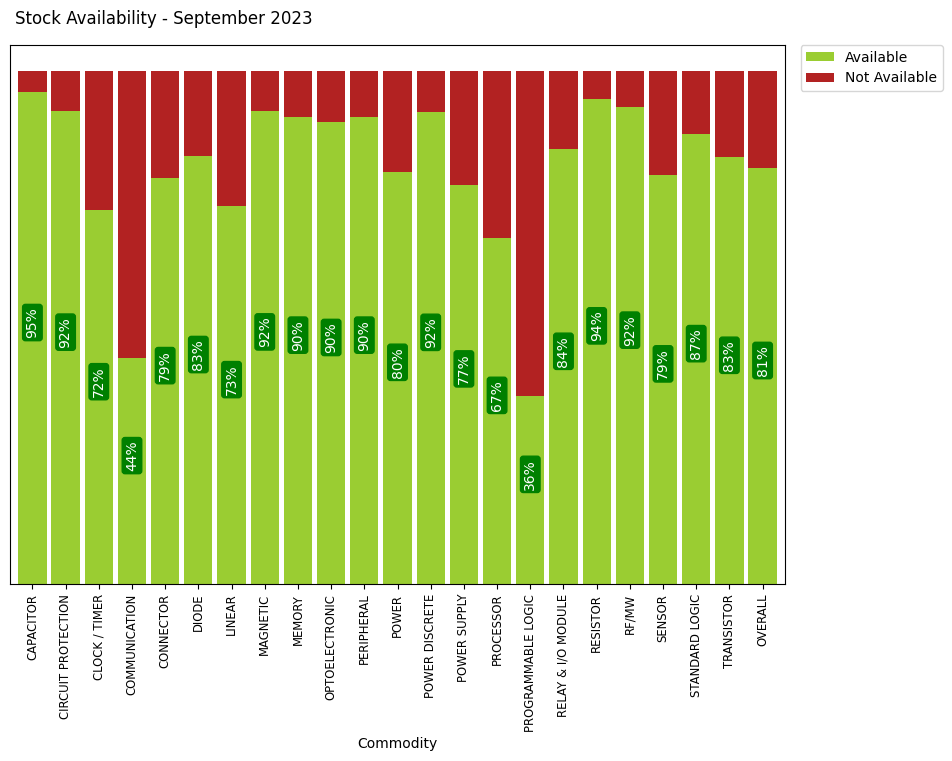

Electronic Component Availability Remains High But Is Moderating

In September, electronic component availability started to moderate with 81% of all tracked electronic components available, down from 84% in August. Those components leading the way from an availability perspective in September included Capacitors (95% Available) and Resistors (94% Available).

.

.

Sign up for our newsletter to get access to our next update for September 2023 – where we’ll see if October’s improved market conditions continue.