One Basket, Two Markets: AI Demand Splits Component Pricing

Lytica is the world’s only provider of electronic component spend analytics and risk intelligence using real customer data. As a result of our unique position in the marketplace, we have been able to work with 100+ customers in analyzing over $550 billion in electronics spend. We curate up-to-date insights into these state of the electronic components market reports and share them with you here each month. Subscribe today to receive these each month upon release.

Lytica’s component basket comprises 165,000 electronic components across more than 30 categories, including the most popular devices used by our customers. These indices are intended to show market trends. Individual component and BOM analysis is offered by Lytica as a service to our customers.

What May’s +1.49% Is Hiding

What is the overall electronic component price trend in May 2026?

In the State of the Market April Report, three forces were still developing: Memory had just posted its sharpest monthly increase to date at +9.50%, the Strait of Hormuz closure and Ras Laffan facility damage had only begun affecting fab-level output, and the report cautioned that the April headline of +1.10% likely understated the disruption because it hadn’t yet worked through to contract pricing.

The May report confirms each of those threads. Memory remains elevated at +8.20%, but the more telling signal is on the supply side: Processor lead times extended by +12.56% and Memory lead times extended by +10.79% in the same month, the clearest evidence yet that the helium constraint has moved from a pricing risk to an active supply constraint. What was forecast as a fab-level disruption “beginning to materialize” in April is now visible in delivery windows, not just price.

The overall price index came in at +1.49% in May, a step up from April’s +1.10% but still below March’s +2.30%. The headline number continues to understate the real picture. Pricing pressure is no longer broad-based; it is concentrating rapidly in AI-critical component categories, while mature, consumer-adjacent segments hold flat or ease. Two markets are operating inside the same basket, and procurement teams whose BOMs skew toward AI infrastructure are experiencing a fundamentally different cost environment than those serving industrial or consumer applications.

The forces driving this divergence are structural, not cyclical:

- AI & Data Center Pull: Sustained hyperscaler investment continues to strain the supply of memory, processors, power management, and optical components, with no sign of demand slowing any time soon.

- Foundry Cost Pass-throughs: Pricing pressure consistent with the late-2025 foundry rate resets at TSMC and other leading manufacturers continues to work through the market, with analog, mixed-signal, and logic categories among those showing the effects.

- Raw Material Costs: Elevated prices for copper, lithium, and aluminum remain a persistent upstream pressure across wire, cable, magnetics, and power components.

- Helium Supply Constraint: The disruption to semiconductor-grade helium supply flagged in March and April is now affecting Memory pricing and Processor lead times. This is now a current risk.

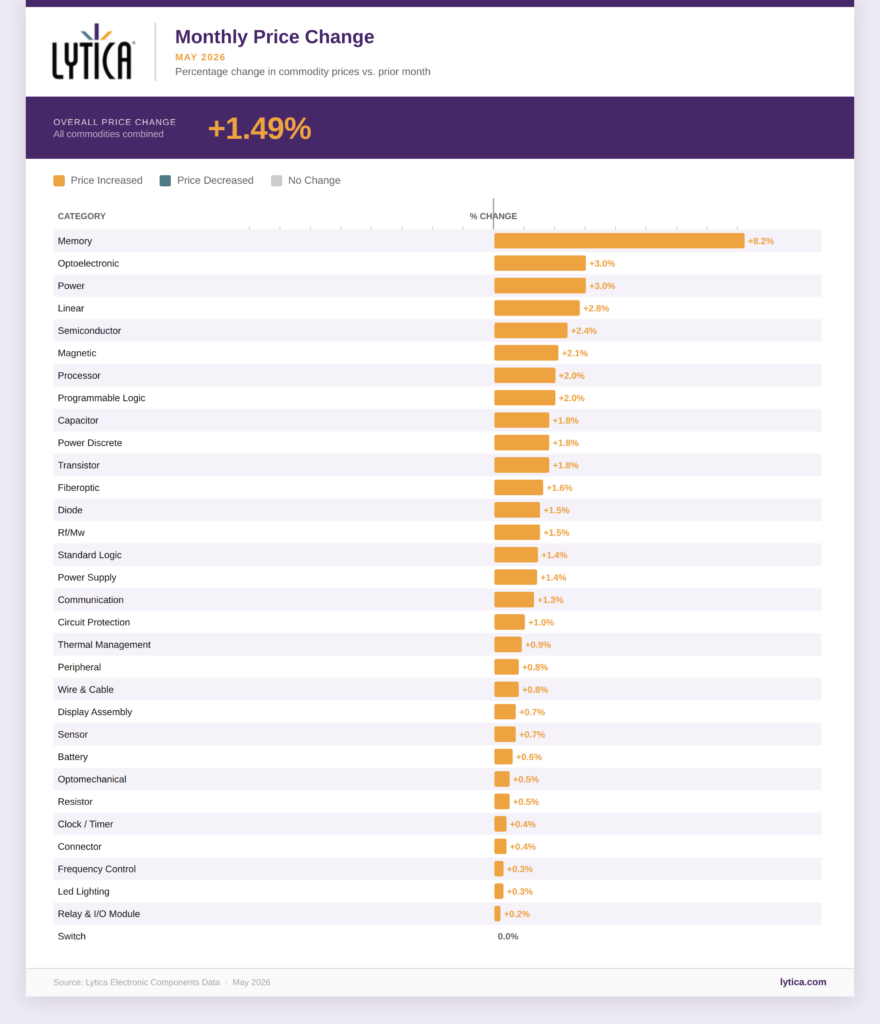

Monthly Price Change by Category

Which electronic component categories saw the largest price increases in May 2026?

Processor lead times extended +12.56% in May — the largest lead time increase of any category this month. Memory lead times extended +10.79%, the second largest. Both categories share direct exposure to the helium supply constraint affecting advanced fab processes.

Teams managing memory-heavy or AI-accelerator BOMs who have not acted on forward contract coverage are running out of runway. Do not use May's overall +1.49% as a planning assumption for H2. AI-critical categories are tracking above the basket average.

Figure 1: Monthly Price Change by Category — May 2026. Source: Lytica Electronic Components Data.

Memory (+8.20%) — Five Consecutive Months of Acceleration

Memory posted +8.20% in May, down slightly from April’s +9.50% peak but still the highest-increasing category in the basket by a wide margin. The April report flagged that Memory availability at 93.66% might need revision as helium constraints tightened fab output; that revision is now confirmed. May availability came in at 91.7%, a measurable decline, and the combination of continued price increases and tightening availability signals that supply constraints are co-developing alongside supplier pricing power. HBM capacity allocation continues to crowd out standard DRAM. Teams without forward contracts may face growing H2 exposure.

Memory at +8.20% in May and availability at 91.7% (down from April's 93.66%). The April report warned of this decline. Both price and supply access are tightening simultaneously.

Optoelectronic (+3.00%) and Power (+3.00%)

Both categories posted +3.00% in May, reflecting the same AI infrastructure investment story. Optoelectronic demand is being driven by the continued expansion of high-speed optical networking inside data centers, the infrastructure that’s increasingly built to support AI and GPU cluster workloads. Power components face sustained upward pressure from EV infrastructure, industrial automation, and AI data-center power-delivery requirements. Neither category shows any signs of reversals.

Linear (+2.80%) and Semiconductor (+2.40%)

Linear reversed April’s decline (-0.30%) to post +2.80% in May, reflecting analog demand recovery from industrial and high-performance computing applications. Semiconductor posted +2.40%, up sharply from -0.10% in April.

Processor (+2.00%) and Programmable Logic (+2.00%)

Processors continue steady inflation at +2.00% in May. Major AI infrastructure leaders continue placing early orders for the processors and servers needed both to train AI models and to power the AI services now reaching everyday users. Because the most advanced chips require ultra-precise, contamination-free manufacturing conditions that depend on helium, processor fabrication is especially exposed to the ongoing helium supply constraint, with no viable large-scale substitute currently available.

Capacitor (+1.80%), Power Discrete (+1.80%), and Transistor (+1.80%)

Three categories posted exactly +1.80% in May, reflecting broad-based upstream cost pressure in passive and discrete components. Wafer cost pass-throughs and sustained demand from automotive and industrial electronics are the primary drivers.

Connector (+0.40%) — April Watch Item: Price Follow-Through Did Not Materialize

April’s report flagged Connector, after March’s lead times spiked +170.73%, warning that price follow-through remained likely. It did not materialize — Connector posted just +0.40% on price in May, with lead times normalizing to +3.49%. One likely explanation is that March’s spike reflected the same procurement front-loading behind that month’s basket-wide lead-time surge, rather than a genuine capacity constraint, which would explain why it cleared without price impact — though that’s not confirmed. Copper-driven cost pressure on Connector remains real, and the category still belongs in Q3 budget reviews on that basis.

Battery (+0.60%)

Battery continues to significantly understate raw material pressure. Lithium carbonate remains near $26,000 per tonne — nearly double year-earlier levels. The pass-through gap will close.

Relay & I/O Module: +0.20% price increase in May despite continued availability tightness at 78.4%. Connector (+0.40%) and Wire & Cable (+0.80%) posting modest gains despite copper above $12,900/tonne. These categories historically lag raw material cost pressure by 30–90 days.

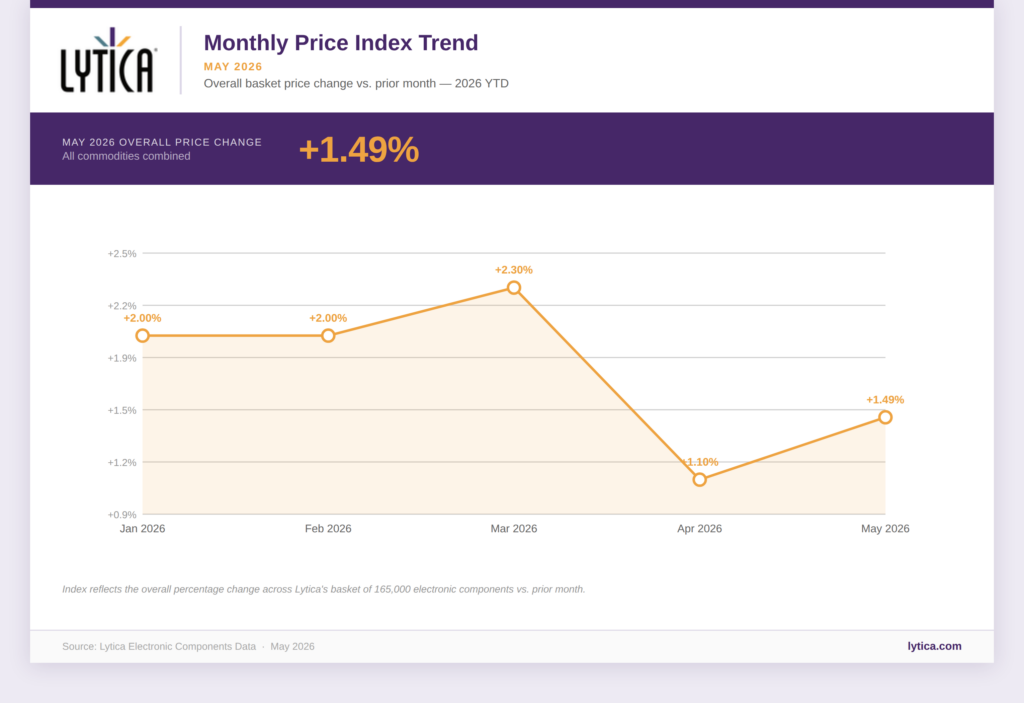

Monthly Price Index Trend

What is the trend in overall electronic component pricing through early 2026?

Figure 2: Monthly Price Index Trend — January to May 2026. Source: Lytica Electronic Components Data.

Five months of data reveal a market that is bifurcating rather than moderating. The January-March pattern of steady, broad-based increases has given way to a more complex picture. April’s apparent deceleration to +1.10% was concentration, not cooling. May’s +1.49% confirms that the basket average is being held down by flat-to-declining mature categories, while AI-critical components continue to inflate.

The spread between Memory’s +8.20% and Switch’s 0.00% is now 8.2 percentage points — the widest category divergence in the 2026 dataset. Procurement teams need to assess their BOM exposure by category, not by the overall index.

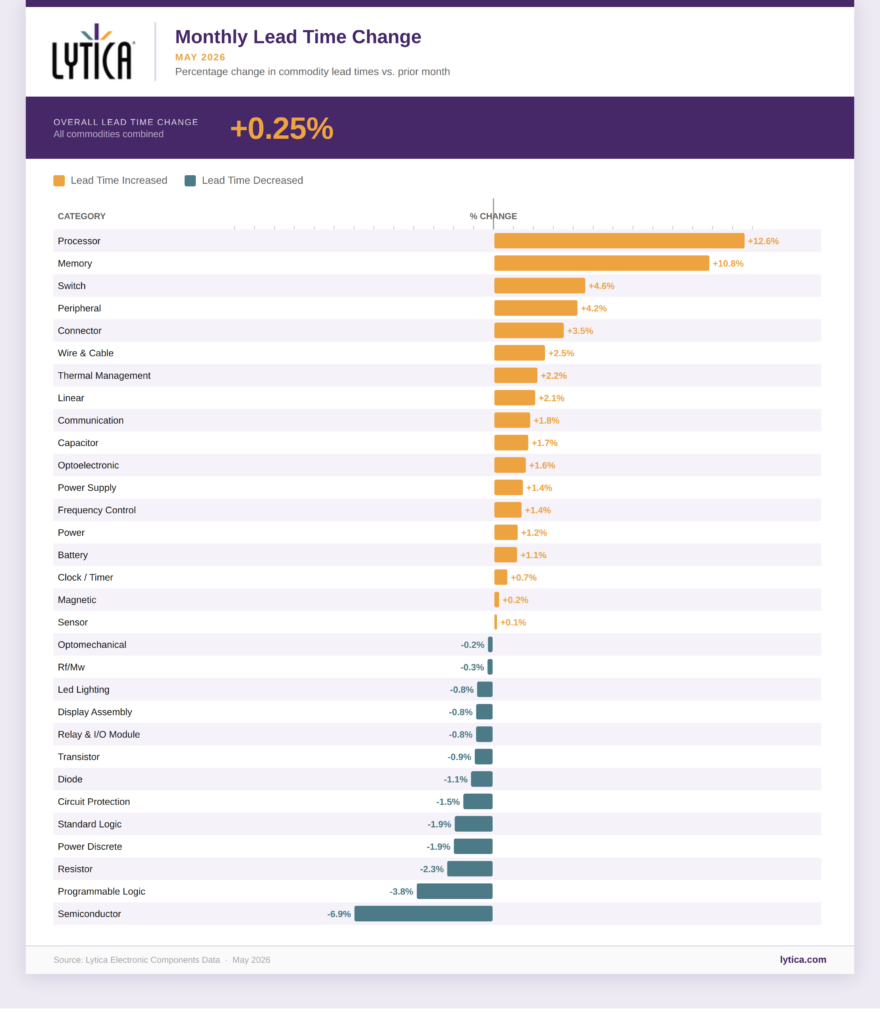

Monthly Lead Time Change

Are electronic component lead times improving or worsening in May 2026?

Figure 3: Monthly Lead Time Change by Category — May 2026. Source: Lytica Electronic Components Data.

Fiberoptic is not shown in this chart. Its May lead time figure matched its stock availability figure exactly, and rather than risk an inaccurate read, we chose to display the remaining categories at a clearer scale this month.

The overall lead time index came in at +0.25% in May, nearly flat — but the basket average masks significant category-level divergence. What remains after April’s normalization is a tale of two groups: AI-critical categories where lead times are extending, and mature categories where lead times are holding or compressing.

The largest lead time extensions in May:

- Processor: +12.56% — the largest lead time extension in the basket. Helium supply constraints for sub-5nm fab processes are beginning to show up in delivery windows.

- Memory: +10.79% — simultaneous price and lead time extension is the defining signal of a supply-constrained, not just demand-driven, inflation event.

- Switch: +4.56% and Connector: +3.49% — modest but consistent with structural demand in industrial and infrastructure categories.

- Peripheral: +4.17% — still extending after April’s +17.83%. April flagged this category for monitoring over 30-60 days. The watch continues — pricing follow-through remains likely over the next 30 days.

Categories posting lead time compression in May:

- Semiconductor: -6.94% and Resistor: -2.28% reflect normalization from prior-month extensions.

- Programmable Logic: -3.81% and Power Discrete: -1.94% — compression consistent with mature category dynamics.

- RF/MW: -0.26% — April flagged RF/MW as a category to monitor for pricing follow-through after lead times extended +13.03% in April. RF/MW lead times compressed in May. This watch item is resolved.

- Relay & I/O Module: -0.83% — lead times compressed in May after extending +28.48% in April (following a +89.45% spike in March). The squeeze pattern flagged in April has partially eased, but availability remains tight at 78.4%, and pricing is still lagging at +0.20%. Continue monitoring.

Processor (+12.56% lead time) and Memory (+10.79% lead time) are extending simultaneously on both price and delivery windows. This is the signature pattern of a supply-constrained market, not merely a pricing cycle.

Peripheral lead times are still extending after April's spike — pricing follow-through remains likely if the pattern holds into next month.

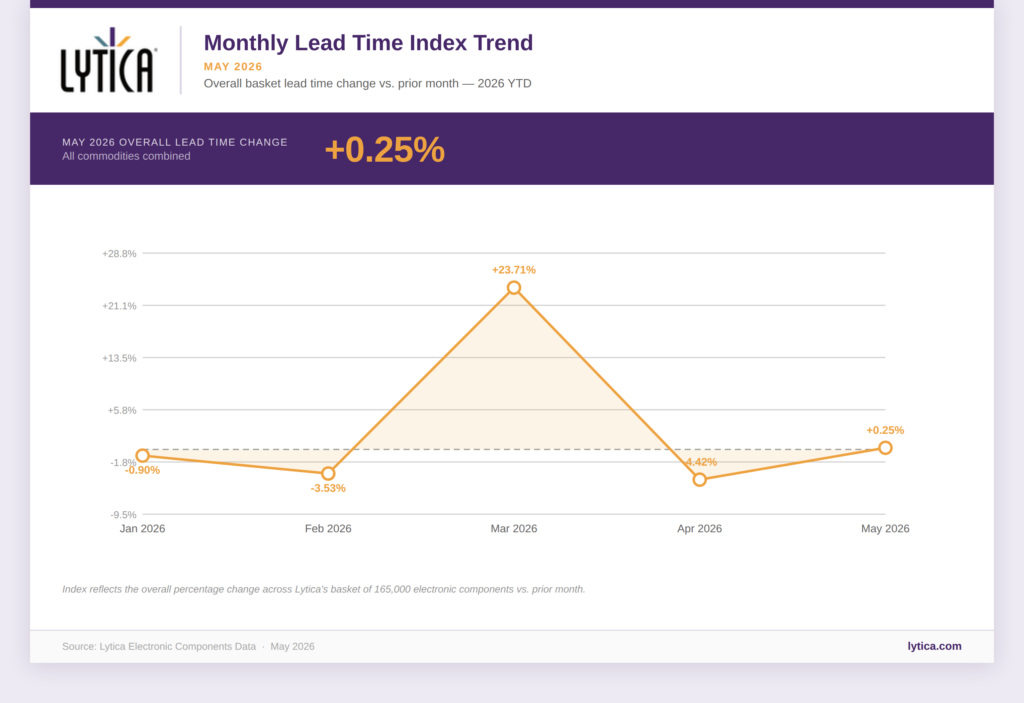

Monthly Lead Time Index Trend

How have lead times trended across 2026 to date?

Figure 4: Monthly Lead Time Index Trend — January to May 2026. Source: Lytica Electronic Components Data.

The five-month pattern tells a coherent story. The broad compression of Q1 signalled a relatively healthy supply. March’s spike was a procurement response to anticipated Q2 price increases. April’s normalization reflected short-cycle inventory dynamics following that front-loading event. May’s near-flat overall index conceals divergence: AI-critical categories extending, mature categories compressing. That divergence is the defining lead time story for H2 planning.

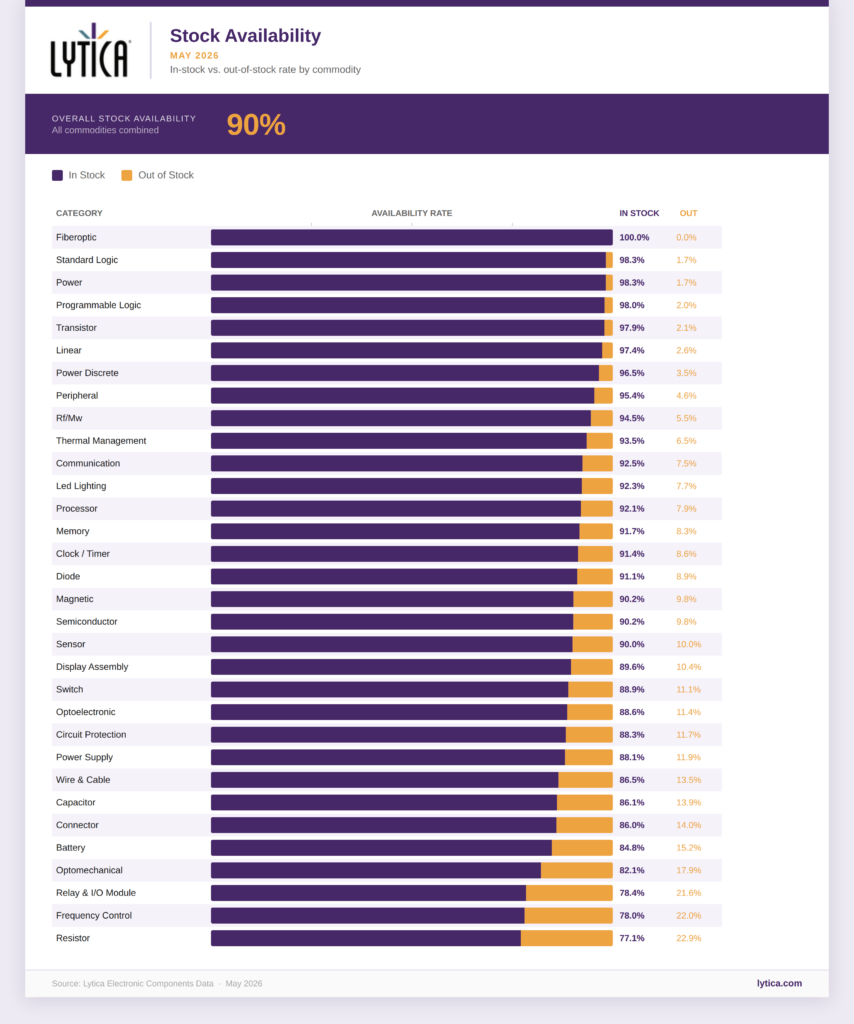

Stock Availability

What is the current stock availability for electronic components in May 2026?

Figure 5: Monthly Stock Availability by Category — May 2026. Source: Lytica Electronic Components Data.

Categories reaching or near 100% availability in May:

- Fiberoptic: 100.0% — Despite strong demand from companies expanding high-speed optical networks in data centers, supply has kept pace, with no signs of backlog or constraint.

- Power & Standard Logic: 98.3% — Both commodities remain well supplied despite consistent price increases. This availability may reflect the power of producer pricing rather than shortages.

- Programmable Logic: 98.0% — This mature category is currently maintaining supply.

Tightest availability categories in May:

- Resistor: 77.1% — tightest availability in the basket this month

- Frequency Control: 78.0% — limited improvement from prior months: watch for pricing catch-up

- Relay & I/O Module: 78.4% — availability tightened from April’s 81.84%, moving in the wrong direction despite a slight lead time compression of -0.83%.

- Optomechanical: 82.1% and Connector: 86.0% — both warrant monitoring

The April report noted that Memory availability at 93.66% supported a cost-driven inflation interpretation and flagged that assessment for revision as helium constraints tightened. That revision is now warranted. Memory availability dropped to 91.7% in May, and simultaneous lead time extension confirms supply constraint is developing alongside pricing power.

Overall basket availability at 90% still supports a broadly healthy supply picture at the basket level. But AI-critical category dynamics are shifting — and the next report will be the first to fully reflect whether that shift is accelerating.

Subscribe now to ensure you don't miss it!Looking Ahead: Key Takeaways for Procurement Teams

What should procurement teams prioritize based on the May 2026 component market data?

May continues the trend we’ve seen in 2026: the electronics component market is operating as two distinct cost environments under a single headline index. AI-critical categories are inflating rapidly and tightening on delivery. Mature, consumer-adjacent categories are holding flat or posting modest increases. Managing a BOM that spans both environments requires category-level planning, not basket-level assumptions.

Specific priorities for procurement teams for the month ahead:

- Memory and HBM — Up +8.20% in May, along with a +10.79% lead time extension. Memory is in a supply-constrained pricing environment. Availability has tightened to 91.7% from April’s 93.66%. Forward contract coverage should be treated as urgent, not discretionary.

- Processor — +12.56% lead time extension is the single most important supply signal in the May report. At +2.00% on price and with sub-5nm helium exposure, Q3 exposure is building.

- Peripheral — Lead times still extending at +4.17% after April’s +17.83% spike. April flagged this for 30–60-day monitoring. The watch continues — pricing follow-through remains likely if the pattern holds into next month.

- Optoelectronic and Power — Both up +3.00% in May with strong availability. AI infrastructure demand is accelerating, not moderating. Include in Q3 budget planning.

- Relay & I/O Module — Partially eased from April’s squeeze signal: lead times compressed and price held at +0.20%. Availability remains tight at 78.4%. Continue monitoring through next month before clearing from the watch list.

- Wire & Cable, Magnetics, Connector — Copper above $12,900/tonne continues to press through these categories. Note that Connector’s anticipated price follow-through from March’s lead-time spike did not materialize in May, but the underlying raw material pressure remains.

- Battery — +0.60% in May significantly lags lithium carbonate raw material costs (~$26,000/tonne). The pass-through gap will close. Build this into H2 cost models now.

|

Sources and References

The following sources were consulted in preparing this report to provide broader market context, pricing data, and geopolitical analysis, in addition to Lytica’s proprietary component basket data.

- TrendForce, Memory Price Outlook for 1Q26 Sharply Upgraded, February 2026

- Counterpoint Research, Memory Prices Surge Up to 90% From Q4 2025, February 2026

- Deloitte Insights, 2026 Semiconductor Industry Outlook, February 2026

- Reuters, Helium Shortage Has Started Impacting Tech Supply Chains, March 2026

- Tom’s Hardware, The global helium shortage is a direct threat to the chipmaking supply chain, March 2026

- Digitimes, Strait of Hormuz disruption puts semiconductor supply chains at risk, March 2026

- Bloomberg, Iran Strike Damages 17% of Qatar LNG for 3-5 Years, March 2026

- Carbon Credits, Lithium Prices Climb Again in 2026, March 2026

- Trading Economics, Copper Price Historical Data, 2026

- J2 Sourcing, The Global Helium Crisis: What It Means for Semiconductor Manufacturing, March 2026

- Frost & Sullivan, Helium as the New Chokepoint in Semiconductor Supply Chain: Can Singapore Turn Adversity Into Opportunity? March 2026

- Carra Globe, Semiconductor Supply Chain Disruption 2026: How the Helium Crisis Is Hitting Chip Fabs, March 2026

- MLQ.ai, Middle East Conflict Sparks Helium Shortages Endangering AI Chip Production, April 2026

- Value Chain Asia, TSMC Helium Shortage and the Semiconductor Supply Chain, April 2026

- Futurum Group, AI Capex 2026: The $690B Infrastructure Sprint, February 2026

- Deloitte Insights, Why AI’s Next Phase Will Likely Demand More Computational Power, Not Less, 2026

- Build Insights, AI Infrastructure Capex in 2026: What Hyperscaler Spending Means for Developers, May 2026