In my last blog, Supply Chain Crash Test, I asked if your supply chain could withstand a tsunami like event that might wipe out many component suppliers who serve supply chains of the OEM or EMS companies that would cause it. I asked you to postulate what would happen if Apple had experienced the Samsung battery problem; this would be a tsunami … do you know the impact it would have on your supply chain?

In the blog, I stated that there are three important things that you need to know about the suppliers and manufacturers in your supply chain:

- Are they likely to be a first round knockout because of a distress zone prediction from an Altman’s Z- Score or Zeta model or other risk scoring equations such as Ohlson’s O-score or Shumway’s simple hazard model?

- If a tsunami like environment impacts their sales, can they raise enough cash to survive for 1 to 2 years while inventory and sales issues resolve?

- Do they have enough customer diversification to turn a tsunami event into a discomfort rather than a death threat?

These are valid questions but getting answers to them is not a trivial task. How do you find out a company’s capacity to raise cash when the underlying conditions used for credit worthiness are altered dramatically with such an event? If you had a diversification metric on each company, how would it be applied? What distress zone prediction score threshold value would indicate a safe zone in the future?

This thought experiment has led me to some interesting insights and a possible solution.

Cash

Cash determines survival; without cash a company can’t pay bills and dies. In a risk analysis, we need to remove things that make companies look good but cannot be converted to cash in an operational setting. Goodwill is at the top of the list and enters the Altman score through total assets. Goodwill is the premium that companies paid during an acquisition that could not be justified by normal accounting valuations. It is the excess amount remaining after all other assets of the company being acquired have been valued. This premium is justified by management through arm waving and claims of combined synergies. It is the missing 1 in the equation 1+1 = 3.

From a risk perspective, recalculate the distress zone prediction score with goodwill set to zero. When stock market prices drop such that the book value of a company is higher than its market cap, goodwill needs to be written off to correct the imbalance. Goodwill is not a real asset in that it can never be converted to cash in an operational action. Do any of your companies fail the test without goodwill? If they do, these manufacturers are at a high risk of failure.

Goodwill isn’t the only thing that impacts a company’s ability to raise cash; diversification sensitivity and resilience also play a role.

Diversification

My company, Lytica, has an advantage. Through our customer BOMs in Freebenchmarking.com we know how broadly a manufacturer and it’s components are used. This gives us a metric for diversification named breadth of use which allows us to distinguish broadly used manufacturers and components from narrowly used ones. Even with this, we can only say that broadly used companies are less risky than narrowly used ones.

Diversification sensitivity

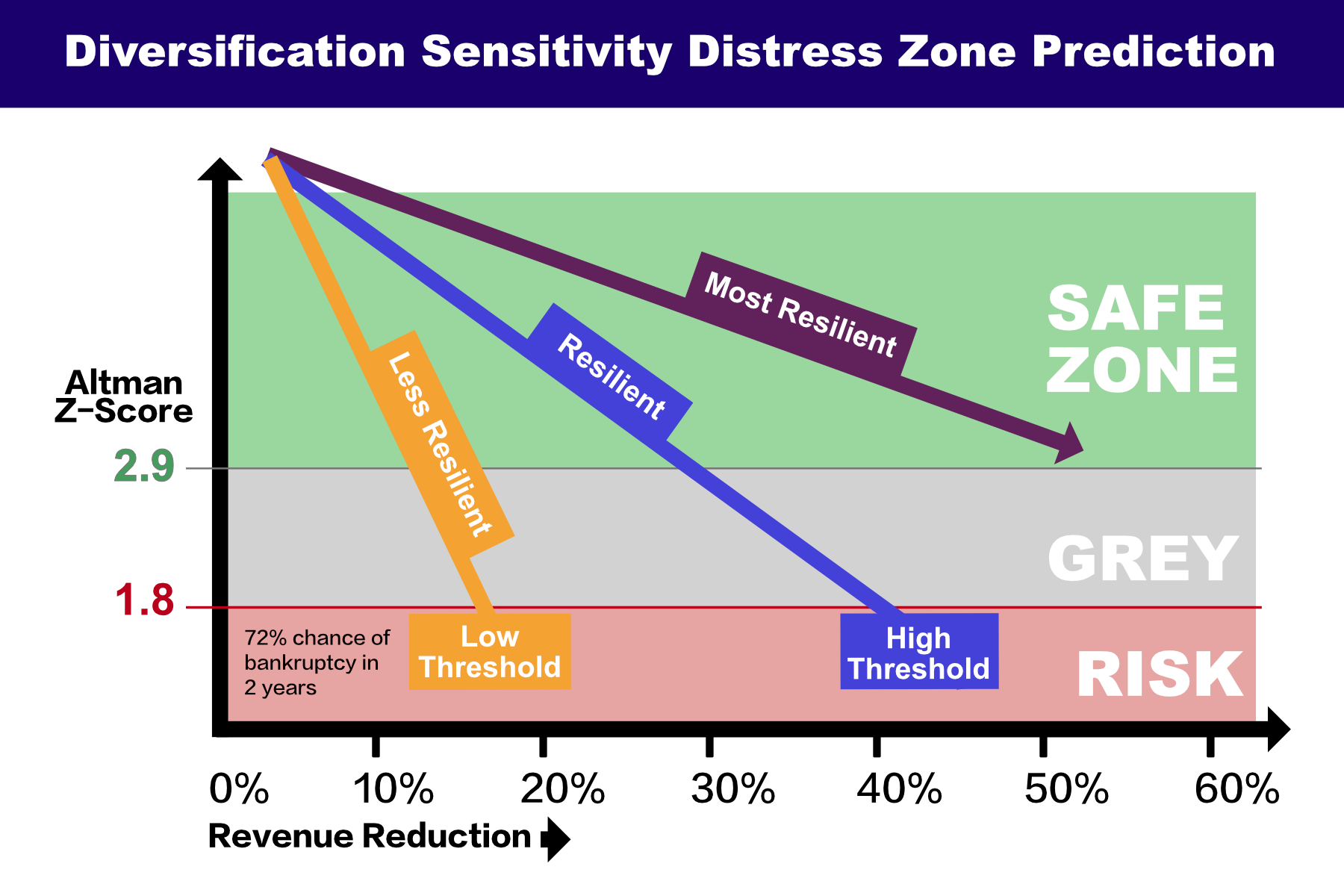

We can however look at the sensitivity to diversification using the profile of a distress zone prediction score like Altman. Let’s assume that 10% of a company’s business came from a tsunami causing EMS. In a tsunami event, 10% of their receivables would be in jeopardy of not being collected and 10% of their inventory would likely be written off or sold at distress levels. If we adjusted receivables, inventory and other directly impacted parameters for the impact of the 10% reduction and recalculated the Altman score, what would it look like?

We could continue this approach in 10% (or some other increments) and plot a curve of these score calculations against revenue reduction. Somewhere on this curve there is likely a threshold score in the distress zone where they won’t be able to raise cash. Where does your manufacturer fail the threshold?

Are these Altman or other distress thresholds still valid? One could argue that if an Altman’s score is valid at any point in time as a catastrophic failure predictor, then these revenue loss scenarios with the resulting scores would be meaningful and the current thresholds valid. Perhaps, but another approach would be to rank like companies (those making the same type of products) and be concerned by those who generate the lowest scores.

In any event, if you can access the financial statements of your manufacturer, you can perform a diversity sensitivity analysis by plotting the score profiles and using them to establish confidence levels in your manufacturers. The shock may come from the loss of a key customer or from a general downturn but the consequence is the same.

Resilience

Not all companies are created equally and their ability to withstand a revenue shock is a measure of resilience. For example, a distributor can shed labour costs faster than a manufacturer can eliminate debt from capacity expansion.

Lytica’s resilience parameter is the inverse of the slope of a best fit line of distress zone prediction scores (Y- axis) plotted against revenue change (X-axis). In this metric, higher scores indicate more resilience and a better ability to absorb shock. The distributor in the example above should be more resilient.

We are currently automating these calculations for hundreds of component suppliers and will be reporting our findings in future blogs.

Ken Bradley is the founder of Lytica Inc., a provider of supply chain analytics tools and Silecta Inc., a SCM Operations consultancy.